(Alliance News) - Stocks in London remained in the red at midday, but outperformed their European peers, as a pick up in UK private sector growth helped offset underwhelming earnings.

Disappointing tech earnings in the US, were followed by lacklustre numbers from LVMH and Deutsche Bank, amongst others, prompting investors to cash in some recent gains.

The FTSE 100 index traded 13.83 points lower, or 0.2%, at 8,154.04. The FTSE 250 was down 58.02 points, 0.3%, at 21,033.47, while the AIM All-Share was down 1.34 points, 0.2%, at 788.83.

The Cboe UK 100 was down 0.1% at 814.04, the Cboe UK 250 was little changed at 18387.51, and the Cboe Small Companies was also flat at 17,244.12.

Kathleen Brooks, research director at XTB, said it is "hard to see how the rally in markets can continue for now after several weaker than expected earnings reports including Tesla, LVMH and [UPS], have led to concerns that stocks will fail to deliver the boost to earnings that would spur the next leg of the rally."

"The slip in corporate earnings from the likes of Tesla and Google, which failed to set the market alight with its AI investments, suggests that the fundamental basis for a rally is slipping away as we reach the peak summer months."

After hours in New York, Google owner Alphabet fell 3.4%, while electric carmaker Tesla slid 7.8%.

Tesla missed Wall Street profit estimates in the second quarter as it repeated guidance that vehicle growth in 2024 would be "notably lower" than 2023. Alphabet highlighted "ongoing strength" in its Search segment, as well as "momentum" in Cloud, after seeing both revenue and net income climb in the second quarter.

However, the YouTube division's advertising revenue fell short of estimates.

On Tuesday, shares in United Parcel Service, often viewed as economic bellwether for the US economy slumped 12% after it lowered guidance.

Stocks in New York are set to open lower on Wednesday. The Dow Jones Industrial Average is called down by 0.4%, the S&P 500 by 0.7% and the Nasdaq Composite by 1.0%.

In Europe, the CAC 40 in Paris fell 1.0%, while Frankfurt's DAX 40 traded 0.7% lower.

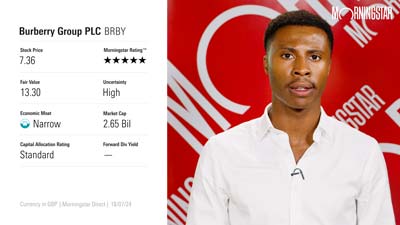

Shares in French luxury conglomerate LVMH, which owns Christian Dior and Tiffany, fell 3.9% after it disclosed a slowing in comparable sales growth. The uninspiring update dragged Burberry down by 1.1% in London.

Weighing on the Dax, Deutsche Bank fell 5.3% after it swung to a loss on litigation costs amid a Postbank lawsuit provision.

Adding to pressure on European stock markets, figures showed the eurozone private sector fell perilously close to a standstill this month, with the manufacturing economy sinking deeper into decline.

The Hamburg Commercial Bank composite purchasing managers' index fell to 50.1 points in July, fractionally above the 50-point neutral mark, from 50.9 in June.

The data "signalled a near-stagnation of the eurozone private sector", survey publisher S&P Global said.

Franziska Palmas at Capital Economics said the data suggests that the eurozone's recovery may be "fizzling out".

The figures were in marked contrast to the UK, where the private sector picked up speed this month, as new business growth surged to a 15-month-high.

The latest S&P Global flash UK composite purchasing managers' index rose to 52.7 points in July, from June's final tally of 52.3, a two-month-high.

S&P Global said the expansion was aided by the "sharpest upturn in new business for 15 months".

The flash services PMI expanded to 52.4 points in July, from 52.1 in June. The manufacturing PMI climbed to 51.8 points, from 50.9.

The services reading was a two-month-high, while the manufacturing PMI spiked to its best level in two years.

Matthew Ryan at Ebury said the figures were consistent "with a UK economy that is growing at a solid, albeit far from spectacular, pace".

"Today's data supports our generally optimistic view on the UK economy, which we think appears primed for an outperformance relative to the rather subdued expectations in 2024. Business and consumer confidence should be propped up by the normalisation in rates of inflation, and the high likelihood of lower Bank of England interest rates, which we expect to start cutting in August. We also see a mild boost to demand from the removal of the election uncertainty and the possibility of closer UK-EU ties under the new Labour government."

The pound traded at USD1.2905 early Wednesday afternoon, down from USD1.2915 at the time of the London equities close on Tuesday. Against the dollar, the euro faded to USD1.0843 from USD1.0855. Versus the yen, the dollar eased to JPY154.70 from JPY155.98.

In London's FTSE 100, easyJet flew to the top of the charts, rising 5.2%.

The Luton, England-based budget airline said it is on track to deliver another "record-breaking summer" following a strong third quarter.

The update was a welcome boost after the warning from RyanAir on Monday which sent airline shares into a tailspin.

British Airways owner, IAG rose 1.2% in response, while Wizz Air edged 0.7% to the good.

Informa climbed 2.2% after announcing the GBP1.2 billion acquisition of Ascential and raising full-year sales guidance.

Informa, the London-based business information publisher and events organiser, expects significant revenue opportunities to arise from the combination, alongside cost savings and efficiency improvements.

Ascential, which revealed the approach from Informa after Tuesday's close in London, jumped 26%.

Reporting half-year numbers, Informa said it now expects revenue for 2024 to be above its previously stated guidance range of GBP3.45 billion to GBP3.50 billion. Revenue in 2023 totalled GBP3.19 billion.

Reckitt Benckiser nudged up 0.7% after announcing a wide-ranging revamp of its business, including the likely sale of a number of well-known brands.

The firm plans to focus on a portfolio of 'powerbrands', such as Strepsils, Gaviscon, Nurofen, Lysol, Dettol, which it defined as high-growth, high-margin businesses that it thinks have the potential for long-term growth.

It plans to sell non-core home care brands including Air Wick, Mortein, Calgon and Cillit Bang, and consider "all options" for Mead Johnson Nutrition, the business behind Enfamil infant nutrition.

Analysts at Citi commented: "While we think the "shrink to grow" story should lead to multiple expansion given the stock valuation anomaly, especially with the Nutrition unit finally put under review, we would flag that this should not be a straight line, as monetizing Mead may require more visibility on the actual potential litigation liability."

In the FTSE 250, Aston Martin shares motored 7.3% higher after it said it is set for a "strong second half performance", despite a widened first half loss.

The Gaydon, England-based luxury sports car maker also confirmed Adrian Hallmark will take over as chief executive officer from September 1, with Amedeo Felisa stepping down on the same date.

Greencore was another share on the rise, up 2.8%, after it raised annual profit guidance, after reporting an improvement in profit conversion in its third quarter.

But Breedon fell 4.0% as half-year profit fell despite higher sales.

The construction materials company said pretax profit dropped 18% to GBP46.5 million from GBP56.5 million.

Among London's small caps, Marston's rose 3.3% as investors cheered news that sales picked up in recent months, with England's run to football's Euro 2024 final lessening the hit from a wet start to the UK summer.

"We have seen considerable uplift from Euro 2024, with like-for-like sales for the week of the semi-final and final matches rising by 8.0%," the pub operator said.

On AIM, Vimto drinks owner Nichols shot up 8.4% after reporting a profit improvement, raised guidance, and a special dividend.

Brent oil was quoted at USD81.58 a barrel, down from USD82.15 at the time of the London equities close on Tuesday. Gold was quoted at USD2,415.35 an ounce, up against USD2,406.10.

By Jeremy Cutler, Alliance News reporter

Comments and questions to newsroom@alliancenews.com

Copyright 2024 Alliance News Ltd. All Rights Reserved.

:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/347BSP2KJNBCLKVD7DGXSFLDLU.jpg)