Eurozone Inflation: What to Expect from July’s CPI Data Consumer prices are expected to have risen by 1.9%, below the European Central Bank’s target. Sara Silano

Global ESG Fund Flows Rebound in Q2 2025 Despite ESG Backlash and Geopolitical Uncertainty Hortense Bioy

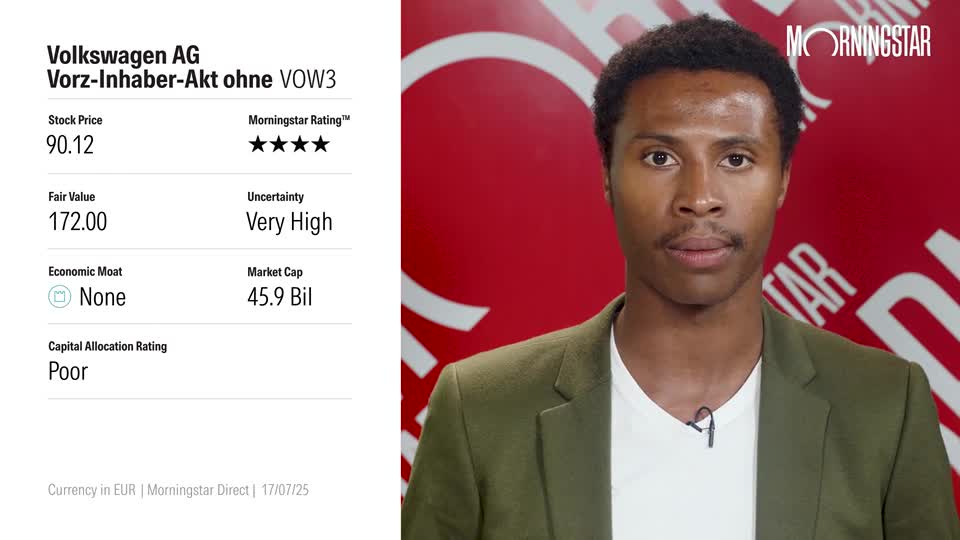

Vodafone: Germany and UK Remain Key Areas of Focus; Maintaining Fair Value Estimate Javier Correonero

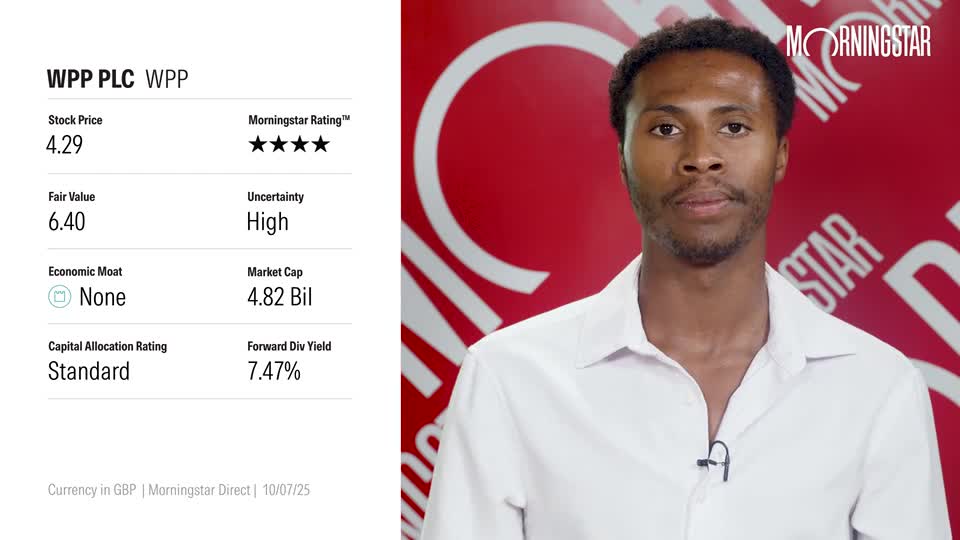

BT Earnings: Executing Well in a Competitive Market; Fiber Rollout and Cost Reductions Tracking Well Javier Correonero

Stellantis Earnings: Gradual Road to Recovery Automotive company expects second-half revenue to exceed the first half. Rella Suskin, CFA

5 Reasons Dividend Investors Choose Funds Over Stocks Ease and flexibility are some of the benefits of investing in dividends through funds. Fernando Luque

Eurozone Inflation: What to Expect from July’s CPI Data Consumer prices are expected to have risen by 1.9%, below the European Central Bank’s target. Sara Silano

Why Gold and Copper Prices May Surge Again This Year Gold, copper, and aluminum are the most promising commodities right now, according to WisdomTree’s head of research. Valerio Baselli

Global ESG Fund Flows Rebound in Q2 2025 Despite ESG Backlash and Geopolitical Uncertainty Hortense Bioy