I’ve had a few thoughts watching bond markets convulse lately.

First, you’d think fixed income would be a good place to be when the Federal Reserve is cutting interest rates. Yet, the Morningstar US Core Bond Index finds itself in negative territory since the Fed made the first of its three cuts in September 2024. Back in 2022, it was interest-rate hikes that inflicted double-digit losses on fixed income. Bonds can’t catch a break!

Second, I find myself reflecting on the prescience of Morningstar’s recently retired vice president for research John Rekenthaler, who wrote “Bonds Are Still Too Expensive” in February 2024. John argued that although bonds had become more appealing after their yields rose dramatically in 2022, those yields were still too low relative to inflation. Equities offered better “real return” potential. When John republished that same article on Nov. 5, 2024, it carried a note: This article was originally published on Feb. 5, 2024. Since it was written, bonds have become slightly less expensive, as 10-year Treasury yields have nudged above 4.3% versus 4.06% in February. The thesis stands, however—particularly given that the economic platforms of both presidential candidates imply high levels of deficit spending. For bondholders, the election was lose-lose. What a good call.

My third thought is that the bright side of the recent bond selloff is that the two major asset classes have moved in different directions. That’s called “negative correlation” and is seen as a positive from a portfolio perspective. Recent losses might be cold comfort for bond investors, but at least diversification isn’t dead.

Trump’s Effect on the US Stock and Bond Markets So Far

Much has been made of how differently stocks and bonds responded to the outcome of the US election. For equity investors, Donald Trump’s victory and a Republican-led Congress meant deregulation, tax cuts, and unleashing of the economy’s “animal spirits.” Not surprisingly then, a postelection stock rally carried into January.

Meanwhile, a very different mood has prevailed in the bond market, where investors worry about profligate government spending, inflation, and interest rates staying higher for longer. A return of the bond vigilantes sent the yield on the 10-year Treasury note from 3.8% at the beginning of the fourth quarter, to 4.5% at the end of 2024, to 4.8% in mid-January 2025.

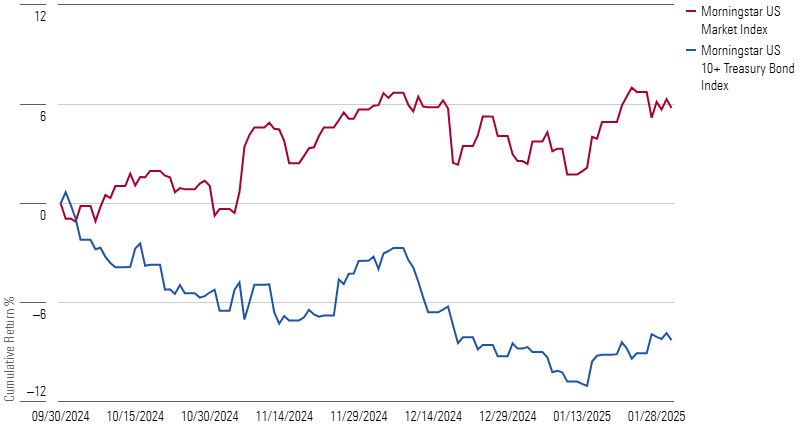

Check out the divergent behavior of the Morningstar US Market Index, a broad gauge of equities, and the Morningstar US 10+ Treasury Bond Index below. Since the end of September, a month in which the Fed reduced its funds rate for the first time in four years, through January 2025, stocks are up, and bonds are down. It looks to me like two asset classes that are “negatively correlated.”

US Stocks Up/Bonds Down

Why is this notable? Well, remember that back in 2022, when inflation moved from “transitory” to “stubborn,” the Fed hiked rates seven times, and stocks and bonds conducted a synchronized swan dive. The Morningstar US Moderate Target Allocation Index, representing 60% stocks and 40% bonds, fell by more than 15% that year.

No one complains when stocks and bonds rise together, but the fact that the two major asset classes suffered simultaneous losses prompted a lot of hand-wringing. The talk that year was of the “death of diversification” and the “end of the 60/40 portfolio.” As my colleague Amy Arnott concluded, high inflation and rising interest rates are typically bad for both stocks and bonds. Correlations tend to rise during such periods.

The Morningstar US Core Bond Index made a nice comeback in 2023—which made few headlines because stocks were up nearly 25%)—but more interesting to me was the behavior of high-quality bonds during equity market selloffs in August and September 2024. As stock investors got a serious case of the jitters, high-quality bonds acted as safe-haven assets and rose in value when equities fell.

“Bonds are So Back,” wrote Jason Kephart, Morningstar multi-asset director of multi-asset ratings in August 2024. It was reminiscent of the diversification benefits fixed income provided during equity bear markets in 2020, 2008, and 2000-02. In each of those periods, the Morningstar US Core Bond Index produced positive returns while stocks were deep in the red.

What’s the Outlook for US Bonds?

From one perspective, it’s hard to get excited about bonds right now. In December, the Fed ratcheted down expectations for rate cuts. “The Fed is likely beginning to incorporate the possibility of inflation-boosting policy changes in 2025, most notably higher tariffs,” wrote Morningstar economist Preston Caldwell in "Fed Sets Stage for Fewer (or Possibly No) Rate Cuts in 2025." We are clearly in tricky terrain.

Ever the contrarians, my colleagues on Morningstar’s Research and Investment teams see the recent bond market selloff as “an opportunity for investors to consider adding moderate-duration exposure by moving out of cash into intermediate-term Treasury bonds.” Back when the yield curve was inverted, investors got paid more to sit in cash than longer-dated bonds. That situation has changed.

Many see bonds as offering decent return potential in the years ahead. My colleague Christine Benz compiles expert forecasts at the start of every year. Some forecasters covered in the 2025 edition expect 10-year returns from bonds to exceed those of US equities.

It’s important to note that enthusiasm for fixed income does not extend to corporate bonds. “Credit spreads are ridiculously tight,” said Morningstar’s Chief US Market Strategist Dave Sekera when we interviewed him for The Long View podcast. Investors are not getting paid to take the credit risk corporate debt carries.

What Should Investors Do?

To me, one takeaway from recent markets is that investment behavior is extremely difficult to predict. We have been reminded that the Fed only controls overnight rates, while the market determines longer-term borrowing costs. Investors who had bet on bonds on expectation of interest-rate cuts have been disappointed.

The good news is that asset class diversification has paid off lately. The past few years have taught us that correlations between stocks and bonds are dynamic. But multi-asset investing has worked in recent months and remains a sensible approach in the face of uncertainty. For investors building portfolios around time horizons, goals, and life stages, bonds remain an important piece of the puzzle.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar's editorial policies.