As most expected, the Federal Reserve cut the federal-funds rate by 0.25 percentage points to a target range of 4.25%-4.50%. The Fed has cut by a cumulative 1 percentage point since initiating cutting in September 2024. Before that, the rate had been on a lofty plateau of 5.25%-5.50% since July 2023.

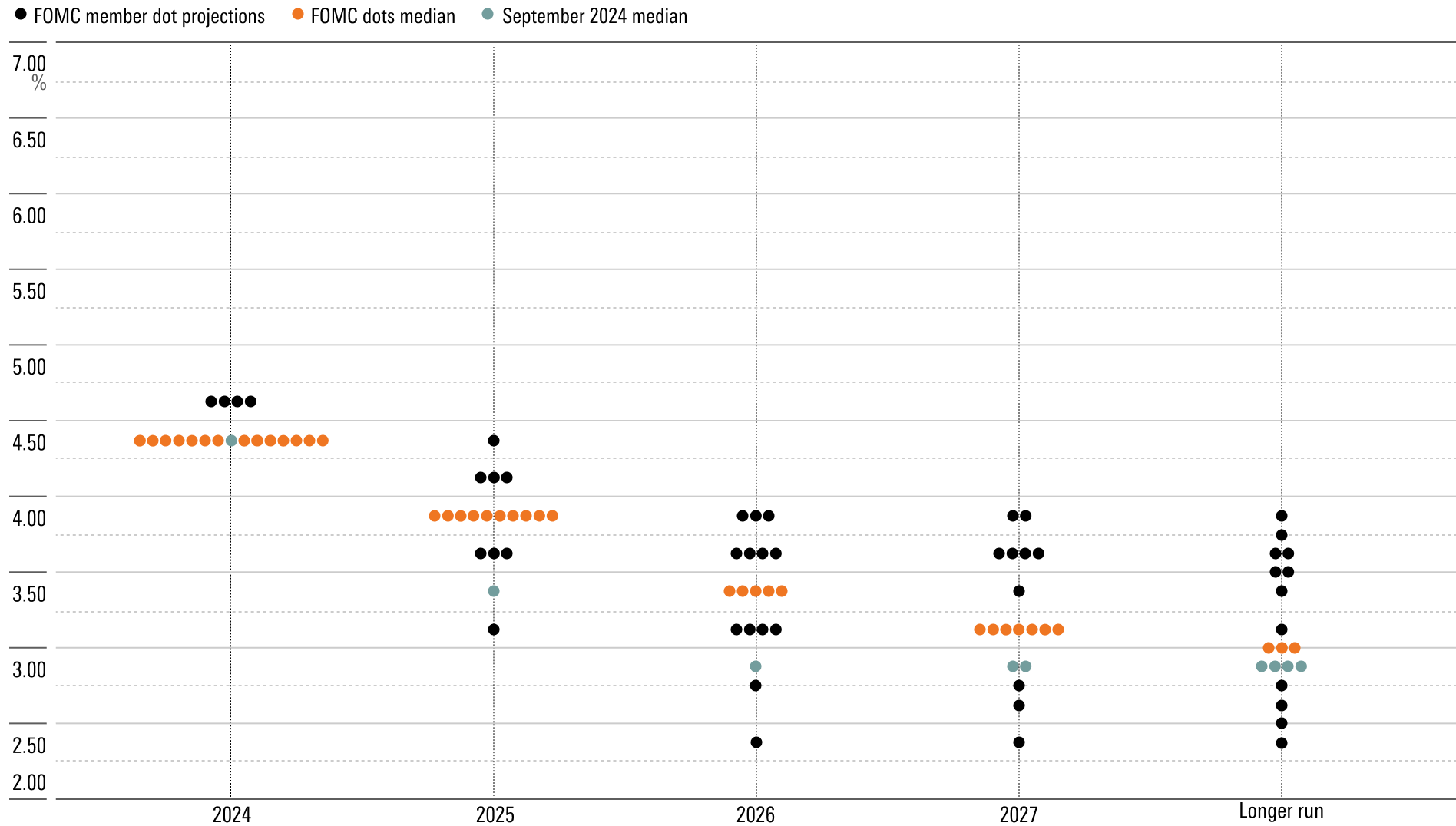

The big news from today’s meeting came from the updated Federal Open Market Committee member projections. The median expectation is now for just 0.5 percentage points of cuts in 2025, versus a full 1% in the prior projections released in September.

The Dot Plot: Federal-Funds Rate Target Level

FOMC participants' assessments of appropriate monetary policy at the Dec. 18, 2024, meeting.

Source: Federal Reserve. Data as of Dec. 18, 2024.

Fed Chair Jerome Powell noted that the federal-funds rate is now “significantly closer to neutral,” although it likely remains “meaningfully restrictive.” The neutral interest rate is consistent with the economy growing in line with its potential, full employment, and inflation in line with the Fed’s 2% target.

There’s much uncertainty about precisely where the neutral rate is located. GDP growth has remained strong despite the Fed’s high interest rates. Inflation is also not quite back to target. As such, it’s unsurprising that one FOMC member voted against today’s rate cut, marking the first dissent since the rate-cutting campaign began in September.

Rate Cut Uncertainty as Labor Market Loosens

On the other hand, the labor market is now somewhat looser than its pre-pandemic state (as noted by Powell). More importantly, the strain from high interest rates on households and businesses’ financial situations is still accumulating, and so downside risk is ever present.

Given the uncertainty about the neutral rate and the vague sense that the federal-funds rate is getting closer to it, the Fed is virtually certain to slow the pace of rate cuts in 2025 to better gauge the effects of monetary policy.

The upward revision in the Fed’s projected year-end 2025 rate appears attributable to its upward revision in projected inflation. It now expects core PCE inflation at 2.5% year over year in the fourth quarter of 2025, versus 2.2% previously.

Inflation-Boosting Policies on the Cards for 2025

The Fed didn’t noticeably increase its GDP forecast, so expectations of higher inflation can’t be attributable to expectations of a hotter economy. Instead, the Fed is likely beginning to incorporate the possibility of inflation-boosting policy changes in 2025, most notably higher tariffs. Powell acknowledged that in today’s meeting, several members explicitly said they were factoring in the possibility of the “economic effects of [new] policies.” Other members were reticent on the topic, but it seems likely to be on everyone’s mind.

Although market expectations were already more hawkish than the Fed’s going into today’s meeting, the upward revision in the central bank’s expected federal-funds rate for the end of 2025 compelled an upward revision in the market’s expectations.

The market is now incorporating a 60% probability that the federal-funds rate target range will be 4.25%-4.50% or higher at the end of 2025, meaning no net rate cuts in 2025, according to the CME FedWatch tool.

Federal-Funds Rate Target Expectations for December 10, 2025 Meeting

Source: CME FedWatch Tool.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar's editorial policies.