In the run-up to the US presidential election we warned that a Trump victory could have negative implications for the European equity market. Despite brushing off some of these concerns prior to the election, in the weeks since, equity markets have been adjusting rapidly as information emerges as to potential policies and implications for stocks.

What has been interesting is the divergence of US and European markets on the election news. Investors in the US are bullish on the prospect of lower regulation and potentially lower corporation tax; US stocks rallied as a result. Meanwhile, an array of potential antagonistic policies vis-a-vis Europe has unsettled European investors, sending the region’s equities into a weeks-long decline.

The list of potential actions directed at Europe is long, but a few impactful examples stand out, all of which could be implemented either immediately or in a matter of just months.

Tariffs on Steel, Aluminum and Autos Target European Producers

During his first term in the White House, tariffs were one of Donald Trump’s preferred instruments around trade policy, with a raft of tariffs introduced particularly in the final two years. They were directed almost exclusively toward China, with the aim to stop the influx of cheap goods to the US.

This time around it is unlikely we will have to wait two years before Donald Trump starts introducing more of the levies. The fact that Trump has already divulged details of potential new tariffs means he’s likely to introduce them soon after his inauguration. The difference being that this time, Europe, as the nation’s largest trading partner, could also be in the firing line.

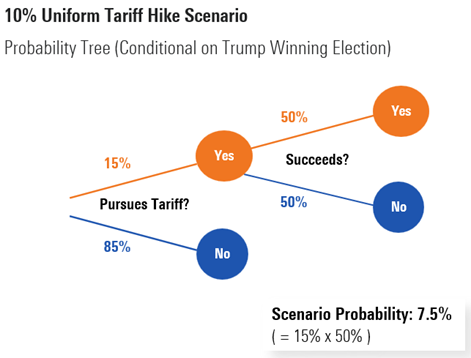

That more tariffs are coming is not in dispute generally, but what is debated is the nature of the potential tariffs. So far, much of the talk has been around universal tariffs, with Trump specifically mentioning a 10% tariff on everything coming into the US.

It is our belief that the probability of such a tariff being implemented is extremely low, at less than a 1 in 10 chance. There is huge opposition from congressional republicans and business groups in the US to such a move. Furthermore, the legal complexities of imposing such a tariff could be significant, with the department of trade likely tied up in lawsuits from business interests for years to come, should it impose the measure.

What is more likely in our view are targeted tariffs. A re-introduction of a charges on steel and aluminum would be easy to implement and could badly hurt European producers like ArcelorMittal MT and ThyssenKrupp TKA, as well as automakers. Europe exports around twice the level of cars to the US that it imports from the US, which Trump has characterized as stealing US manufacturing jobs. For European auto makers with large US revenue exposure like Stellantis STLA or Volkswagen VOW3, this could spell bad news.

Trump’s NATO Threat

With republicans in charge of the House and Senate, getting some tariffs passed should be a relatively straightforward task. What works even more quickly than tariffs are threats. Earlier this year, Trump issued a threat to underspending NATO nations that he would not protect them if they are attacked. Nations not meeting NATO’s 2% of GDP spending target on defense are breaking the agreement, the logic goes, so why should other nations stick to mutual defense obligations?

Defense spending has risen significantly over the last decade, with the advent of the Ukraine war prompting many European nations to up their game. Of the 32 NATO countries, all but 7 are now meeting their promises on spending.

European aerospace and defense stocks were one of very few sectors to rally on the US election result, with the likelihood that it will prod the laggards into action and boost weapons makers' order books. European defense names have had a great run over the last few years, but we believe there is more to come, with the majority of our coverage in 4 star territory, making it an attractive area for investors.

Canceled Subsidies Endanger European Utilities

President Biden’s inflation reduction act offered subsidies to firms investing in renewable energy projects, with around $300 billion set aside for this cause alone. Donald Trump’s opposition to renewable energy is well documented, and the prospect of canceled subsidies has contributed to the underperformance of renewables stocks such as Vestas VWS and Orsted ORSTED since the election.

European utilities were one of the sectors that experienced the largest share price falls on the back of the election result, and with good reason. These firms are some of the largest investors in US renewable energy, particularly wind energy projects. Should this part of the IRA get canceled, they face losing 10%-40% of those projects’ value.

The risks to the sector are material, but so far we have not seen any clear direction on what exactly will happen. There are some mitigating factors- notably, upwards of 80% of renewable energy projects approved under the IRA are based in Republican areas.

Unlike other sectors such as defense and autos, where we view almost the entire subsector as undervalued, valuations in the utilities sector vary massively, with one and five star stocks sitting alongside each other. Despite the risks, we believe many stocks within the sector, like RWE RWE and Engie ENGI, are sufficiently attractive to invest in.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar's editorial policies.