After two years of high interest rates, Jerome Powell’s Federal Reserve is now pivoting to easing monetary policy. The Fed’s decision Wednesday implies that the main battle against high inflation has been won, and all that’s left is mopping up.

The Fed reduced the federal-funds rate to 4.75%-5.00% in its September meeting, down from 5.25%-5.50% previously. Markets had been split on whether the Fed would opt for its normal 25-basis-point cut or go with a 50-basis-point cut.

In the end, the Fed went with the larger cut of 50 basis points. But that doesn’t mean the Fed was trying to deliver a shock to the markets.

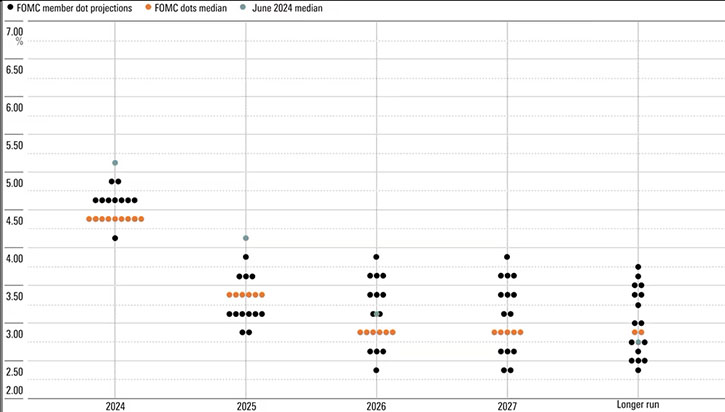

Indeed, the updated FOMC projections imply that the Fed is going to switch to a more gradual pace in future meetings, including cutting by 25 basis points in the final two meetings of 2024. Additionally, Fed projections call for a year-end 2025 federal-funds rate of 3.25%-3.50%. While that’s a hefty reduction from prior projections of 4.00%-4.25% at end-2025, it’s a step above recent market-implied expectations of a 2.75%-3.00% federal-funds rate at end-2025.

In effect, the Fed is suggesting that the market has already baked in ample expectations of Fed rate cuts, and there’s no need (for now) for those expectations to fall further.

Expectations for the federal-funds rate are the primary driver of bond yields. As rate cut expectations have steepened, the two-year Treasury yield has dropped to 3.6% as of mid-September from 4.5% in late July 2024. The 10-year Treasury yield has also fallen by about 50 basis points over that period. This matters because the level of bond yields across the curve is even more important than the level of the federal-funds rate for determining the overall impact of monetary policy on the economy.

Bond yields hardly moved on Wednesday’s decision, evincing the Fed’s desire to not upend current market expectations.

How to Justify a Big Interest Rate Cut?

Still, this raises a question: Why did markets and the Fed shift so drastically toward thinking more aggressive rate cuts were appropriate? In the past few months, we’ve seen mild inflation data continue to roll in. Powell noted that overall PCE inflation was likely to be 2.2% year over year for August, almost in line with the Fed’s 2% target. Meanwhile, the labor market has become more concerning, with unemployment rising by over 0.5 percentage point in the past 12 months and nonfarm payroll employment growth decelerating. Economic activity is still expanding at a healthy pace according to the gross domestic product data, although anecdotal data from the “Beige Book” survey is more concerning.

Altogether, Powell noted that the “risks to achieving employment and inflation goals are in balance,” after high inflation being the overwhelming concern over the past two to three years. To elaborate, that means that ongoing concerns about bringing inflation back to the Fed’s 2% target (which would call for restrictively high interest rates) are equally balanced by concerns that the economy and labor market could slip into a recession (which would call for low interest rates).

Where Next for Interest Rates?

With those two factors in balance, that calls for a federal-funds rate much closer to its “neutral” level. The exact level of neutral is uncertain, but it’s thought to be around 2%-3% according to Fed officials. Cutting by 50 basis points makes more sense when considering the large divergence between a 2%-3% neutral rate and the preexisting federal-funds rate north of 5%.

We think the federal-funds rate is likely to follow a course about in line with today’s FOMC projections, at least through the end of 2025. This amount of monetary easing should be sufficient to keep the economy out of a recession. The uptick in unemployment is far from alarming in our view. With GDP still growing solidly, we find it hard to believe that the labor market is going to spontaneously lurch off a cliff. This should keep the Fed’s cutting to a more measured pace in future meetings.