After a period of decent returns and low volatility, sustainable bond funds struggled in the high interest rate era. Now, as central banks like the ECB start to cut rates, the outlook is improving.

Europe, where nearly half of all global green bonds were issued in 2023, is at the centre of this recovery - recent fund flow data has shown investors returning to this asset class.

Mara Dobrescu, head of fixed income analysis at Morningstar, explains that green bonds have a higher-than-average duration, which reflects a bond's senstivity to interest rate changes. This can be painful when rates rise sharply, but benefits bonds when rates fall, she says.

"Investors looking to invest in green, social and sustainable bond funds should be mindful of the biases these funds may introduce in their portfolio," she adds.

What Are Green Bonds?

Green bonds are issued to raise money for the sole purpose of financing new or existing projects or activities that have a positive impact on the environment. These projects can include renewable energy, energy efficiency, waste management, sustainable transport and other green initiatives.

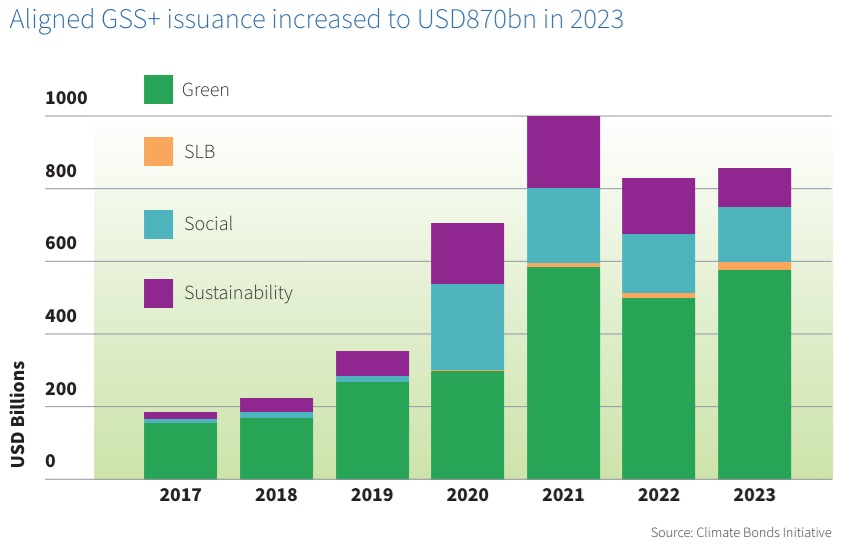

Some $870 billion in new sustainable bonds were issued globally in 2023, pushing the outstanding amount at year-end towards a record $4.4 trillion, across over 43,000 individual bonds worldwide, according to data from the non-profit Climate Bonds Initiative.

Green bonds continue to account for two-thirds of this sustainable bond market.

However, there are other types of sustainable bonds: social bonds, for example, are intended to finance new projects and refinance existing ones, with a positive social impact. The projects are most commonly aimed at supporting low-income, unemployed or otherwise vulnerable parts of the population.

Meanwhile, sustainability-linked bonds (SLB) have structural features, such as interest rates, that are linked to the achievement of sustainability goals.

Unlike green bonds, they are not linked to the realisation of a single sustainability project. The proceeds from the bond issue can be used for general purposes, linked to an overall sustainability strategy with targets that can be measured year by year. These bonds are the most 'generalist' category within ESG fixed income in that they can include environmental targets, social targets or a combination of both.

Funds and ETFs Exposed to Sustainable Bonds

There are just under 300 bond funds and ETFs in Europe that are classified under Article 9 by the SFDR, the European Union’s regulation on sustainable finance that came into force in March 2021. These are those strategies that focus on a 'clear sustainable objective' and are informally called 'dark green' strategies.

In the first four months of the year, these funds recorded EUR 4.2 billion in net inflows, marking an organic growth of 5.4%, higher than the 3.3% growth of the total universe of Europe-domiciled fixed income funds. By the end of April, they reached EUR 75 billion in assets under management.

Morningstar ratings give a useful indication of how these strategies have performed in the past (Star Rating) and how Morningstar analysts think they might perform in the future (Medalist Rating) relative to their category peers.

Another characteristic of these funds is their greater exposure to the euro. An investor who decides to switch from an allocation in traditional global bonds to one exclusively in sustainable bonds would see their exposure to euro issues almost triple to 61%, at the expense of US dollar issues, which would fall to 26%.

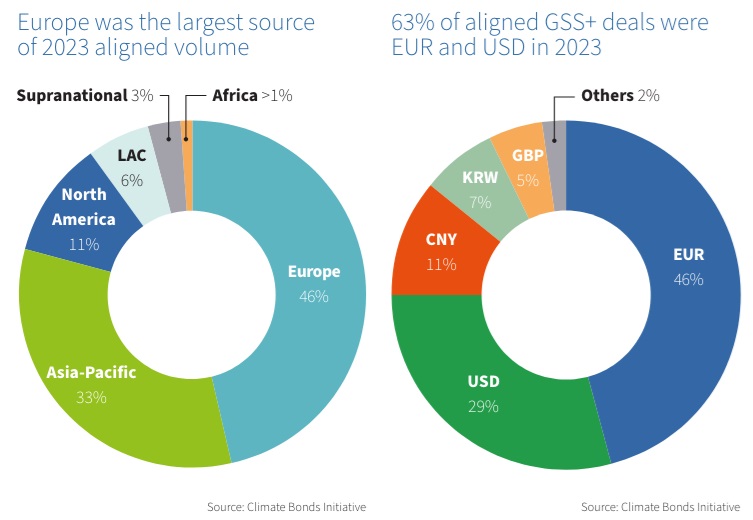

The central role of Europe was confirmed again last year: it was the largest source of sustainable debt instruments with a volume of $405 billion, representing 46% of the 2023 total. Latin America and the Caribbean recorded a 49% year-on-year surge. In contrast, anti-ESG sentiment affected the US volume, with a 38% decline.

At the individual country level, however, the 2023 ranking has China in the lead with $83.5 billion of green bonds issued, followed by Germany at $67.5 billion and the US at $59.9 billion.

Green and sustainable bond funds tend to have higher allocations to corporate bonds, particularly in the financial sector, and quasi-sovereigns, at the expense of traditional government bonds. “This can cause them to struggle more than conventional bond products when credit markets stumble,” Morningstar's Dobrescu warns.

Governments Issue Bonds For Trains and Houses

According to the GSS Bond Report analysis by MainStreet Partners, a global record in green sovereign bond issuance was reached in 2023, exceeding $160 billion. “Clean transportation is the sector most financed by government issuers, to date accounting for 43% of the cumulative volume issued since 2012 - more than three times as much as the category most financed by the remaining part of the market, renewable energy,” the study states.

Belgium's 2018 green bond partly financed the railway system, while in France the proceeds were partly dedicated to tax exemptions for renewable energy and biodiversity projects. In Asia, on the other hand, in response to increasing levels of urbanisation, green bonds are often used to finance sustainable housing projects.

Early Days for Sustainable Bond Funds

Driven by institutional investors, the green bond market should experience continued growth in the years to come. Investors need to pay attention to each issue's quality and be wary of marketing promises.

Selectivity and transparency actually help to ensure that the most relevant and impactful green projects receive the necessary funding. The market remains in its infancy and plagued by greenwashing, so in-depth research on issuers is crucial for investors.