Puig, the Barcelona-based beauty giant that owns brands like Jean Paul Gaultier, has taken Europe by storm in Europe's first continental IPO of 2024 – ending a listings drought and lighting up the luxury agenda once more.

But the business is also making headlines for the leadership style of its chair Marc Puig.

The Catalan businessman running the 110-year-old family-owned beauty group has openly called for his family's "self-disempowerment."

This is a stark difference from Europe's biggest family-backed conglomerates, ranging from LVMH (LVMH) to Kering (KER), where succession plans have entrenched family control.

Puig, however, has made it clear that the fourth generation of his clan, including his own children, will not be involved in running the company.

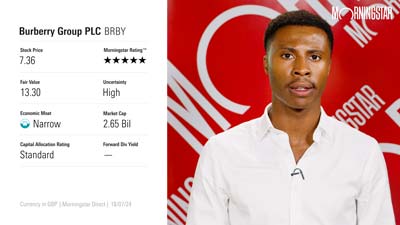

Morningstar consumer equity analyst Dan Su agrees Puig's steps show he is dedicated to injecting professionalism, transparency, and accountability into the business.

"It makes a lot of sense because beauty is a global market and it involves a lot from skin science, fashion trends to manufacturing, to distribution and logistics," she says.

"By including more professional management into the talent pool the company is doing itself a favour in building a high-quality management team to move the company forward."

XTB financial analyst Javier Cabrera is not surprised either, despite the profitability family-owned brands in the luxury space have achieved in Europe.

"It is true: you must have some control mechanisms in place, even if there is not an advisory board that may or may not have executive powers," he says.

"[There must be] people who are in touch with how the business works so the family cannot act solely in the interest of benefiting their holding."

As a case in point, Cabrera highlights the controversy surrounding the Spanish global healthcare group Grifols, which has been accused of manipulating its debt and earnings through transactions to a company connected to the Grifols family.

"Because of this Marc Puig wants to show that he is transparent to the market and to show that something like this cannot happen at Puig," he says.

Despite this, the Puig Family still retains 71.7% of the group and 92.5% of the governing rights. It is also a managing shareholder of the group and its minority business partners in affiliate businesses Charlotte Tilbury and Byredo.

A Welcome End To Europe's IPO Drought

The flotation of Puig Brands, which also owns Paco Rabanne, Chartlotte Tilbury, and Christian Louboutin, made headlines when the company debuted on La Bolsa de Barcelona last week at €24.50 (£21.11).

The listing, which valued Puig at €13.9 billion (£11.98 billion), is the largest float in Europe this year and the biggest Spain has seen since 2015.

The business now holds the number 15 spot on the Spanish Stock Exchange for its size, which makes it a clear candidate to enter the IBEX-35, Spain's top equity index.

Su says it's fair to think shares have been flat-ish since the debut, though she remains bullish on the business's core fundamentals.

"Its share price is not going up a lot from the IPO level," she says.

"But from the Spanish market perspective this IPO generates a lot of interest because the Spanish Stock Exchange is not one of the bigger ones in Europe. So, it was interesting that they decided to list in Spain.

"It is probably fair to say Puig is a high-end beauty company. That is how the company has positioned itself. I would say the competitors for Puig in this case are more likely to be L'Oreal and Estée Lauder, which are both very strong in the premium beauty space, and there is a little bit of competition with Coty."

Are Puig Shares Attractive?

Cabrera believes Puig's shares are quite expensive for a newly-listed business, but reflect the significant growth it has already achieved, especially in 2022 and 2023.

"If the company continues to grow at a double-digit rate above 15%, it will be trading on a multiple that it deserves without a doubt, especially because the returns on invested capital are quite high. In 2023 they were returning around 30%.

"In Puig's case, they know how to bring in a new company, they know how to maintain the core nucleus of the business, and that includes the family members that may be behind the acquired company, while finding a way to integrate them into the wider business.

"That alignment of interests between Puig and the company that was acquired, is noticeable, and it makes the brands keep working in the right way."

In the last century, Puig expanded into fragrances propping itself up as a manufacturer for other brands such as Carolina Herrera. But Marc Puig pushed for the firm to acquire companies in fashion, make-up, and skincare, which now account for more than 90% of all of the firm's sales.

At the time writing Puig Brands is trading at €26.00 (£22.34).

.jpg)