.jpg)

European equities have risen to within a few percentage points of their fair valuations. The road ahead may be getting steeper.

The second quarter saw markets tick upwards, recovering some of the lost ground from the March banking crisis and associated sell-offs, but the progress has been slow and gradual against the backdrop of a worsening macroeconomic environment.

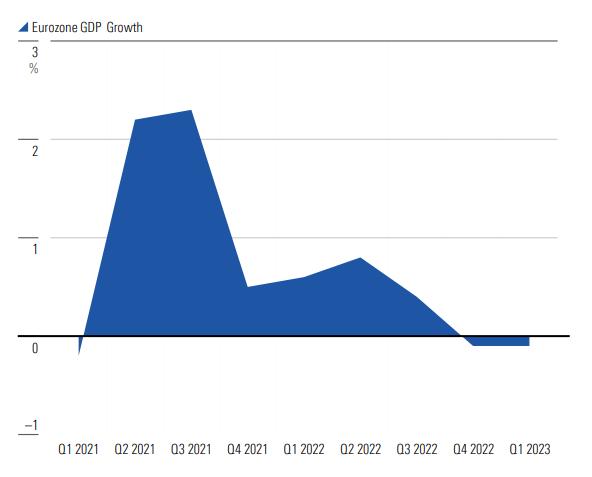

Inflation is certainly falling-- slowly if you live in the UK-- but moving in the right direction at least. This has come at a cost: Interest rates stand at 5% in the UK and 4% in the Eurozone, the highest levels since before the global financial crisis. This is unquestionably having a negative impact on business, with the Eurozone already in a technical recession and the UK very likely to join it this year.

Revisions to GDP Growth Mean the Eurozone is Officially in a Recession

Source: Eurostat. Data as of May 31, 2023

Yet, market valuations have been holding up despite the dark macroeconomic clouds, something we put down to investors leaning on the longer-term picture. We usually complain that the market is too short-term focused, but for once this doesn’t appear to be the case. Investors cling onto hope for an improving economic environment later this year or into 2024, when inflation may finally fall enough for central banks to take their feet off the interest rate accelerator. The danger here is that inflation could remain elevated for longer than investors anticipate, sending interest rates high enough to put the economy into tailspin.

Morningstar European Coverage Average Price/Fair Value Estimate by Sector

Although European equities are very close to our fair value estimate, we see some clear opportunities in specific sectors. Consumer cyclicals, telecoms, and financial services are particularly unloved at the moment, while the European energy stocks remain at a discount to their US peers.

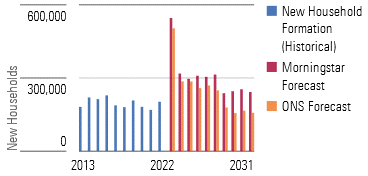

Thematically there are some bright spots too. Rising interest rates in the UK have not been kind to the country's homebuilders, whose stocks remain far below their 2021 highs. Investors are clearly worried about reduced demand for housing as the cost of borrowing increases, but taking a longer-term view, we see an ageing population and continued population growth as structural drivers of demand.

Housing Demand To Stay Robust As Population Ages

Meanwhile, valuations are stretched in the insurance sector. My colleagues recently sought to answer the big question of whether the industry is next in line to suffer from rising interest rates, following banks' troubles in the first quarter. Its challenges include:

- Rising number of claims

- Rising cost of claims due to inflation

- Interest rates reducing the value of their investments

- Rising cost of debt

Although we don’t anticipate a major blow-up across the sector, we do believe that investors need to be more cautious than ever, paying particular attention to insurers' balance sheet robustness when picking stocks.

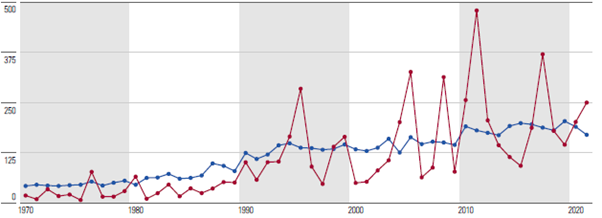

The Number of Natural Catastrophes and Damage Being Caused Continues To Rise