Multi-asset funds have been out of favour for a number of years, but a new Morningstar study suggests that investors should re-appraise the category in higher interest rate environment and higher yields from bonds and shares.

According to Morningstar fund analaysts Bryan Cheung and Tom Mills, multi-asset income funds now face a more attractive opportunity set, especially with the improved outlook for fixed income.

For one, these funds provide diversification benefits without their managers taking on excessive risks. They’ve also proved their resilience in volatile market conditions like last year, when the best funds outperformed the wider falling market.

Here we show the biggest UK funds in this sector.

What Are They?

Multi-asset funds are a "one-stop" shop for investors to get a diversified portfolio from a range of assets including equities, bonds, commodities, cash and currency.

Income-focused iterations focus on regular income and capital growth. They are generally not the highest yielding funds or the best performing at the end of every year, but they offer a flexible approach to asset allocation depending on market conditions.

They are also useful to fund investors in this way because they tend to avoid the "hero to zero" approach, where top performers like tech funds in 2020 and 2021 became the bottom performers in 2022 after the value rotation.

From fund flow data, it’s clear that some investors tend to chase league tables after periods of outperformance, leading to underperformance the following year.

"They can respond to a changing market environment by adjusting their allocation between growth and defensive assets and access a wide set of income opportunities in various asset classes," Cheung and Mills say.

Managers also have "multiple levers to pull" to achieve this balance. The recent trend has been to shift exposure towards higher quality and investment grade bonds, which offer lower yields and lower risk – bonds with lower credit ratings typically offer higher yields to compensate for the higher risk of default.

The Back Story

As the authors say, multi-asset income funds became popular after the 2008 financial crisis as yield became harder to come by. These funds seemed to offer "the best of both worlds", with a steady income stream matched by active management to take advantage of (generally favourable) market trends.

In the low interest rate environment, investors had to take on higher risk in the search for yield. But some of this pursuit has increased the fragility of the funds during market downturns. Now multi-income managers don’t need work as hard for yield as interest rates have soared.

In the UK, for example, 2-year gilts now yield 5.16%, up from 1.99% a year ago. This has fuelled wider investor interest in bonds, which are highly inflation-sensitive assets. But as bond yields rise, their prices fall; for a primer on how the asset class works, see What is a Bond?

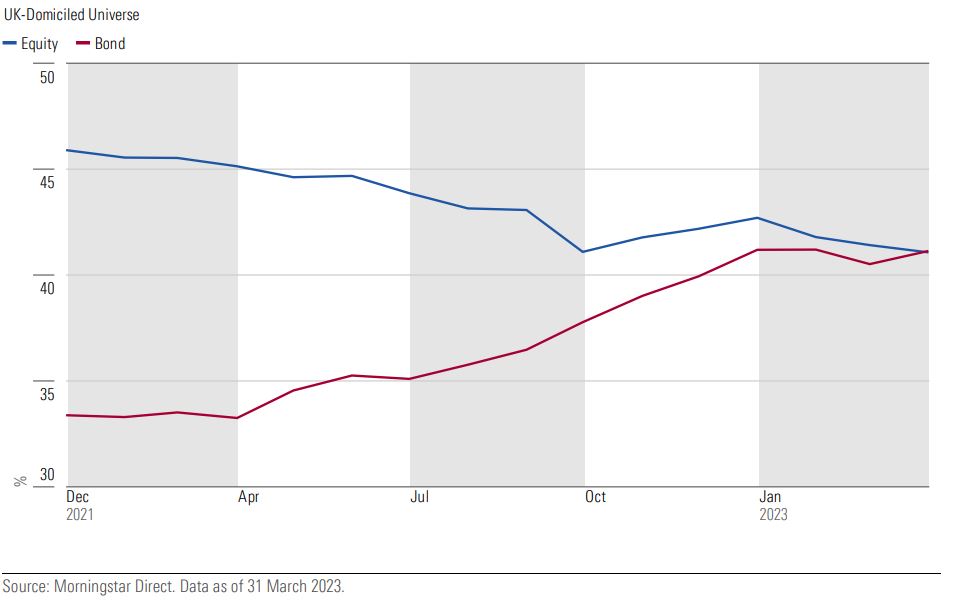

As you can see, the UK funds in the survey have substantially increased their bond exposure since December 2021, when interest rates hit their cylical lows. Equity exposure has falled in that period but is still above 40%.

These funds have managed to weather tough income environments such as 2020, when UK equity income funds were hit by the wave of dividend cuts and cancellations. UK equity income funds have fallen out of favour in recent years for a number of reasons, but in the UK multi-asset income funds have also seen net outflows since 2018.

"These multi-asset income funds can provide a more stable income stream by diversifying their sources of income, which was shown in 2020 when some provided relatively resilient income despite significant reductions in equity dividends in certain markets, including the United Kingdom," Cheung and Mills say in their report.

2022 was harder because the traditional "60/40 equity/bond portfolio" – the template for many multi-asset funds – had one of its worst years in history because equities and bonds fell in tandem.

This goes against conventional investing experience and data, which relies on the idea of bonds providing some support when equity markets wobble.

Multi-asset funds were able to cushion some of this downside, however, and didn’t perform as badly as benchmarks, some of which fell by around 20%.

What Are The Alternatives?

Higher yields on cash and money market funds are drawing investors in because they appear to offer low or no risk to capital while also providing tempting, but not inflation-beating yields.

After a period when cash offered 0% interest, some accounts are now offering upwards of 5%. The report’s authors caution against switching out of multi-asset income funds for yield, especially as cash and money market investments offer no capital growth.

"They do not offer upside potential beyond their yields, and hence, investors have a dismal chance of beating inflation over time," Cheung and Mills say.

Money market funds are also exposed to potential rate cuts – when central banks eventually stop hiking – and there’s something called "reinvestment risk" because they need to reinvest their underlying securities continually.

A Note on Income

Multi-asset funds quote "distribution yield", which is a similar concept to "dividend yield", but different in a crucial sense because it also includes capital gains.

These funds collect income and capital gains from their various asset classes to pay out to investors. Some of our funds generating their payouts largely from income, but others lean more heavily on capital gains.

Cheung and Mills discuss this in detail but their findings can be summarised as follows:

"Higher payouts come with more risk-taking, either via allocating to higher-yielding securities or securities with higher total return potential such as growth equities to fund the distributions.

"In an upward-trending market, it may work fine as long as capital gains keep up. However, when markets turn sour and asset prices fall, high payouts can exacerbate the risk of capital erosion. Continued capital attrition typically leads to falling distribution amounts over time, even if the distribution yield remains unchanged."

So capital gains can make a big difference to the money investors actually receive.

Are They All the Same?

Our analysts say investors need to understand what their funds' risk/returns profile really are, because they can differ considerably in terms of their asset mix and how they go about generating this income. Choosing a fund that matches an investor's objectives and risk tolerance is key, Cheung and Mills say.

Methodology

The authors looked at the largest funds in the UK-domiciled universe (as well as Asian funds). The survey’s fund size and performance data is to the end of April 2023 but we’ve updated this with more recent data.

The authors used only funds with a 12-month track record of paying income. Most of the UK funds provided a yield between 3% and 4%, which is lower than some global alternatives.

Of the 79 funds in the survey, 15 yielded more than 5%, 26 yielded between 4% and 5% and 38 offered yields between 3% and 4%. The research found that the funds offering the highest payouts performed less well than those offering more modest yields.