The UK housing market is in a very fragile state.

House price declines are accelerating and mortgage rates have risen sharply as the Bank of England continues to hike rates in the face of stubbornly high inflation.

As a result, mortgages themselves are harder to come by, and lenders are being tougher as economic conditions tighten. Houses are now also much more expensive to build. After a golden decade of strong returns, shares in London-listed housebuilders reflect this malaise and short sellers have started to circle. But are investors being too pessimistic?

Yes, according to Morningstar’s latest report on the sector, authored by analysts Grant Slade and Ava Gams and titled UK Homebuilders: Built on Solid Foundations, Not Shaky Ground. They look at the long-term drivers of UK property demand and select the stocks most likely to benefit.

A Crash Coming?

If interest rates are yet to peak, some experts are expecting worse to come in terms of house price falls. Some are even calling for a crash to "rebalance" the market after strong capital gains since the global financial crisis of 2008-2009.

Morningstar’s Slade and Gams say an all-out meltdown in prices is unlikely, however, because of ongoing demand for rental property. Interest rates are also forecast to peak this year and then start to fall – so mortgage costs will too.

Nevertheless, house price growth is likely to moderate in the medium term to around 3% a year, Slade says, and that’s below the long-term average. Housing in general is fairly valued rather than extremely overvalued, which would imply a correction.

The current data is confusing – building society Nationwide reported a monthly fall in house prices in May, but that follows a rise in April. Year-on-year house prices are weaker. What’s troubling investors at this stage of 2023 is that the trends are pointing downwards.

Slade says the housing market is at a cyclical low after a long period of growth, but that current valuations imply that the market will never recover.

Beyond 2023

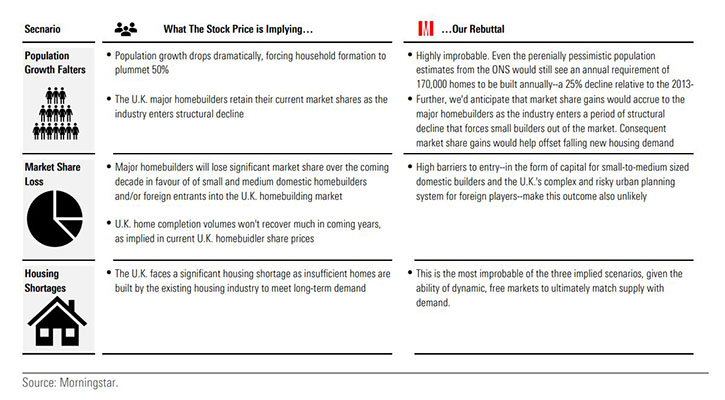

As well as house price falls, what troubles investors and weighs on housebuilder valuations at this point is the idea that current home sales volumes will be significantly lower than the average of the last 10 years – a scenario our analysts think is "highly implausible". In contrast, they expect house sales to bounce back meaningfully over the coming decade.

One key argument for this recovery hangs on demand. The supply of homes has for many years failed to keep up with the number of people wanting to buy them. This is set to continue, with successive governments unable to trigger the "right" housebuilding levels.

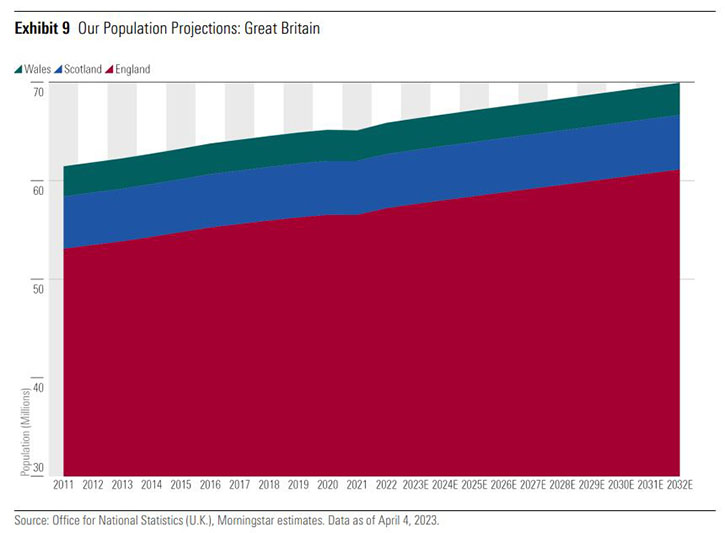

Modelling Office for National Statistics (ONS) data on demographics, our analysts forecast population growth will continue to support housing demand in the coming decades. Net migration figures were above 600,000 last year, significantly above forecasts.

"We think that net migration will be stronger over the coming decade than the ONS projections suggest, noting that its net migration projections have perennially undershot actual migration figures," they say.

Another swing factor is the expected rise in single-person households in the future, which will also support requirements for more housing stock. So we’ve got a combination of an ageing population (more people), higher migration to the UK (more people) and smaller households (more property needed) all combining to make a compelling bull case.

Housebuilding Stocks

Why will listed housebuilders be able to capitalise on these demographic trends, rather than, say, smaller bespoke constuction companies? The answer is multi-faceted.

"Existing market shares, extensive land development experience and inventories of greenfield land held for future development, coupled with expertise in navigating the UK's unique urban planning system make us confident that they will continue their significant contribution to new housing supply in the coming housing cycle," Slade and Gams say.

In terms of the companies Morningstar covers, Persimmon (PSN) is the pick because of its focus on cheaper housing and proven track record of shareholder returns. With "affordability constraints" likely to continue – in plain English, people will struggle to buy at current prices – desire for better value housing is expected to stay strong.

"Persimmon is unique amongst its major homebuilder peers, focusing on first homebuyers in the lower value segment of the housing market where it delivers homes priced well below the UK average house price. Its differentiated model has delivered for shareholders over the long-term," they say.

Persimmon’s peers Taylor Wimpey, Barratt Developments and Bellway all screen as undervalued too, despite some recovery in share prices this year after a bruising 2022.

A Bad 2023, Then a Recovery?

Our analysts don’t shy away from the difficulties faced by listed housebuilders this year.

"With dramatic financial tightening bringing the prior decade's worth of rising house prices and home completions to an end, the 2023 outlook for UK homebuilders is grim," they say.

"Volumes are expected to contract meaningfully as homeowners are shied away from the housing market by the marked increase in mortgage interest rates. Equally, profit margins are under significant pressure as higher interest rates create a headwind to house prices at a time when inflationary pressures continue to soar."

Still, the biggest homebuilders are in a strong financial position to ride out the current crisis, with low debt or even positive cash positions. This compares favourably with how many went into the last financial crisis, which was another cyclical low in the housing market that preceded a recovery in prices.

"With UK homebuilders under our coverage well-positioned to ride out the near-term turbulence, investors stand to benefit from taking a contrarian position," they say.

James Gard is senior editor at Morningstar

.jpg)