It's spring, and Europe finds itself with more than double the gas in storage it had at this time last year. In its effort to dodge a nightmare scenario of economic and humanitarian crisis during the past winter, it's been so successful, it may be on course for a gas glut by the end of the decade.

Milder temperatures and the gas price shock during the first months of war helped in this dramatic shift, however, policy-driven changes were vital. Record additions of wind and solar capacity supported the power grid and EU emergency measures curbing gas demand proved successful.

Combined inventories in the EU were equivalent to 625 terawatt-hours (TWh) on March 21, according to data from Gas Infrastructure Europe or GIE, which accounted for 55.6% of the full capacity, up from just 25.7% a year earlier.

During 2022, natural gas demand in the European Union fell by 55 bcm, or 13%, its steepest drop in history, according to the International Energy Agency. The decline is the equivalent to the amount of gas needed to supply over 40 million homes, and the trend has continued in 2023.

Lower demand helped depress gas prices from an all-time high of €340 last August to €42 at the end of March. The only time in history Europe had even more gas in storage at the beginning of spring was 2020, when a collapse in global demand due to the Covid pandemic had pushed front-month futures below €9.

A Future Without Russian Gas

This puts Europe in a position of strength to meet its pledge to eliminate all Russian fossil fuel imports by 2027. Pipeline supplies have already been crimped to 7% from 40% before the war, according to think tank Bruegel. As we highlighted in a prior part of this series, this isn't the full picture though: While pipelines were shut, imports of Russian liquefied natural gas (LNG) increased by 50% during 2022. The EU's pledge includes ditching Russian LNG.

Russia has squandered its energy exports as a tool of political coercion, but continues to profit from Europe's gas consumption.

“We can and should get rid of Russian gas completely as soon as possible, still keeping in mind our security of supply,” the European Commissioner for Energy Kadri Simson said during a meeting of EU lawmakers on March 9. “I encourage all member states and all companies to stop buying Russian LNG, and not to sign any new gas contracts with Russia once the existing contracts have expired,” Simson emphasized, adding that this could also reassure other gas suppliers Europe is trying to negotiate deals with.

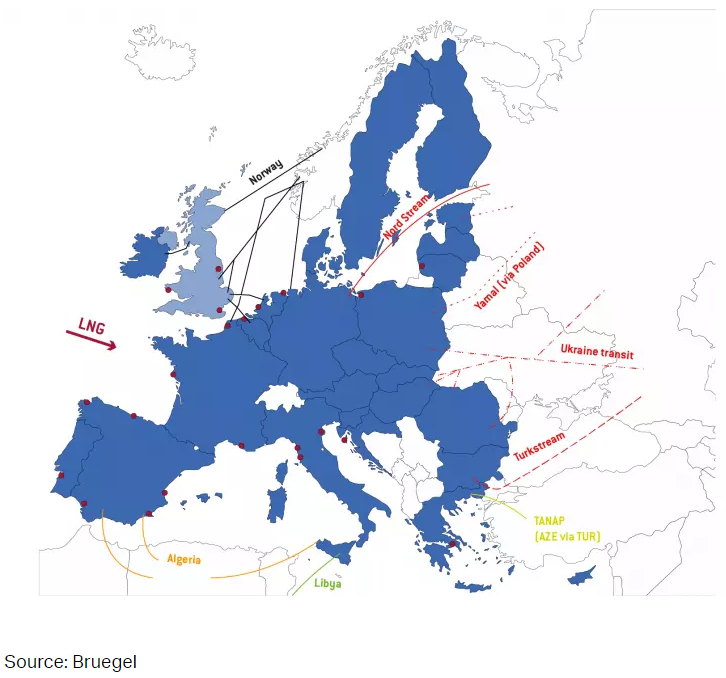

The map below displays the most relevant pipeline import routes into the EU and the location of LNG terminals. The largest share of gas used to be delivered from Russia via four distinct corridors: Nord Stream and Yamal, via Poland, have been shuttered while some deliveries continue through Ukraine and via Turkstream.

Main EU Natural Gas Imports Routes

How much is too much LNG?

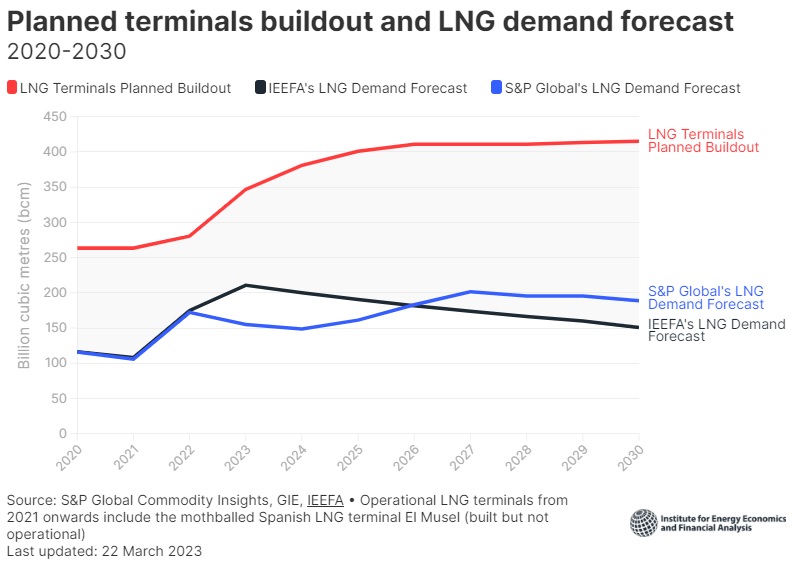

The EU is on course to double the number of its import terminals in order to process rising shipborne deliveries. This will be crucial to plug a supply hole left behind by Russian gas, but may also result in twice as much import capacity as Europe needs by 2030 as renewables keep gaining market share.

According to a new analysis by the Institute for Energy Economics and Financial Analysis (IEEFA), European countries risk wasting huge sums of money on gas import infrastructure they won’t need once the crisis will be gone. Europe’s infrastructure network consists of 31 operational LNG import terminals; besides that, 32 LNG import terminal projects are currently under construction or in the planning stage.

“On one side, countries have felt the need to build more LNG regasification terminals to import gas from other sources to guarantee a secure source of energy. But on the other hand, the crisis has also shown Europe's great dependency on fossil fuels and has encouraged the development of more renewable energy projects, as well as the implementation of energy efficiency methods and demand mechanisms to reduce gas consumption”, according to the analysis.

According to the research, there’s a big discrepancy between forecasted LNG demand in Europe and new regasification capacity being built and planned. Rapidly growing capacity contrasts against an outlook of steady demand.

IEEFA forecasts a 19% increase in LNG demand in 2023, followed by a 5% decline in 2024 and sharper declines thereafter. Assuming the REPowerEU plan is delivered on schedule, the think tank expects gas demand in the region to drop 40-45% below 2019 levels.

That means Europe’s LNG terminal capacity could exceed 400 billion cubic metres in 2030, based on current infrastructure plans, while demand may range between 150 bcm and 190 bcm, according to IEEFA and S&P Global Commodity Insights.

The study sees the utilization rate of Europe’s LNG terminals at just 36% by 2030. “This is the world’s most expensive and unnecessary insurance policy. Europe must carefully balance its gas and LNG systems, and avoid tipping the scale from reliability to redundancy. Boosting Europe’s LNG infrastructure will not necessarily increase reliability—there’s a tangible risk that assets could become stranded,” says Ana Maria Jaller Makarewicz, author of the analysis and Energy Analyst for IEEFA Europe.

Near-term opportunities

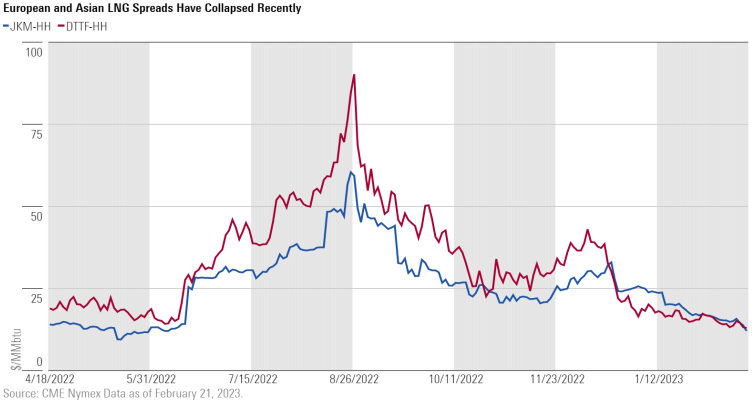

The success the EU has had in lowering gas consumption has reduced the short-term call on U.S. LNG to close supply gaps. The resulting price decline has caused U.S.-EU gas spreads to collapse, meaning lower marketing profits for American firms.

Stephen Ellis, energy & utilities strategist at Morningstar, believes U.S. LNG still has a large role to play in the coming winter, and sees opportunities in exposed stocks this year.

“We continue to think the market is somewhat shortsighted with its focus on the U.S. dynamics”, continues Ellis. “The EU has yet to address the material gap between supply and demand fully. Our earlier estimates entering the winter seasons suggested a gap of 60-70 billion cubic meters, but with success to date in reducing consumption and higher storage, it looks like that gap is closer to 20 to 40 billion cubic meters today, as the EU is exiting winter with materially more bonus gas in storage than it would typically do so.”

Ellis believes the market is assuming consumption reductions and mild weather will resolve the supply gap ahead of the upcoming winter like it did in the past one, but he remains skeptical: “Either way, as EU gas demand begins to increase in the winter of 2023, and U.S. LNG export capacity increases in 2024, pulling U.S. gas production to the coast, we think the market will start to look much stronger, and investors would be smart to take advantages of any bargains in the meanwhile”

“From a stock perspective, we think 2023 will present a potentially very good opportunity to acquire high-quality names leveraged to gas demand at a discount”, Ellis writes. “We favor companies such as Kinder Morgan (KMI), Williams (WMB), Cheniere (LNG), and TC Energy (TRP).”

Just like gas-adjacent stocks, Europe's exchange-traded commodities have sold off as gas prices sank to a level last seen in August of 2021.

Gas prices are likely to rebound if Europe's goldilocks scenario of the past winter isn't repeated this year. Ellis's team sees U.S. gas prices increasing beyond their $3.30 per mcf midcycle pricing in 2024 before returning to more normalized levels over time as EU gas demand and its need for U.S. LNG declines.