Even after the more than 9% rally for US stocks in July, we continue to view the broad US equity market as materially undervalued, albeit less cheap than it was at the beginning of the quarter. According to a composite of the valuations of the almost 700 stocks we cover that trade in the US, the market is now at an 11% discount to fair value.

Equity markets bottomed out in mid-June and then remained in a trading range until mid-July as investors awaited second-quarter results. Earnings were mixed as a few high-profile misses sent some individual stocks plunging. But quarterly results were generally not as bad as the market had expected.

Even more importantly, though, management teams did not throw in the towel on the second half of 2022. Company executives looked to dampen expectations but largely failed to make wholesale reductions to their earnings outlook for the remainder of this year. With valuations at already low levels following the selloff in late spring and early summer, this provided the market with enough confidence to start reallocating capital back into equities.

Key Takeaways for the Stock Market Today:

- The US equity market is materially undervalued;

- Overweight value and growth stocks, underweight core stocks;

- Communications and cyclical sectors are the most attractive;

- Headwinds expected to begin dissipating in the second half of 2022.

US Stock Market at 11% Discount to Fair Value

In our Q3 outlook, we noted that we thought US equity markets were becoming oversold and that since 2010, stocks had rarely traded at as great of a discount to their intrinsic value. In fact, in mid-June, stocks were trading at their greatest discount to our long-term, intrinsic valuations since the emergence of the pandemic in March 2020, and the growth scare that sent stocks lower in December 2018.

On a longer historical time frame, the only other instance when our price/fair value metric had dropped lower was in the fall of 2011 amid fears that the Greek debt crisis would spread to other countries.

Following the rally in the second half of last month, as of July 29, the broad US equity market is trading at an 11% discount to our fair value.

As measured by the Morningstar US Growth Index, growth stocks surged 14.2% in July, well outperforming the broader market.

Following this gain, these shares are now trading at a discount similar to value stocks, whereas core stocks remain closer to fair value. As such, we continue to favor a barbell shaped portfolio split between overweighting value and growth stocks and underweighting core stocks. The Morningstar US Small Cap Index slightly outperformed in July, rising 10.1%, and small-cap stocks remain the most undervalued by market capitalisation. Large- and mid-cap stocks performed in line with the broader market and both categories are similarly undervalued.

Look to Cyclicals

Across our sector valuations, communication services remains the most undervalued part of the market by far, trading at a 33% discount to fair value, followed by several cyclical sectors that had suffered the brunt of the selloff over the past few months. Defensive sectors, which held their value better to the downside, are fairly to overvalued.

Of note, over half of the market capitalization of the communications sector is concentrated in Alphabet (GOOGL) and Meta Platforms (META). Following earnings, we lowered our fair value on Alphabet by 6.1% to $169 to account for near-term weakness. However, we think the market is extrapolating this short-term weakness too far into the future. Even after cutting back our fair value estimate, the stock remains in 4-star territory and trades at a 32% discount to our intrinsic valuation.

We also lowered our valuation on Meta by 9.9% to $346 following poor second-quarter results and weak guidance. Similar to Alphabet, we think the market is overly pessimistic regarding Meta’s long-term outlook.

For example, based on Meta’s continuing user growth, we believe the company's network effect remains intact, which is the basis of our wide moat rating. We expect further monetization of its Reels product along with an economic turnaround to return top-line growth to the low- to mid-teens range beginning in the second half of 2023. Meta’s stock trades at less than half of our intrinsic valuation, placing it deep in the 5-star rating category.

Also of note in the communications sector, we lowered our valuation of Twitter (TWTR) to $44 per share. We had moved our fair value to Elon Musk’s buyout offer of $54.20 after the company accepted his buyout offer. But following his filing to terminate the deal we have revised our valuation, which is now based upon the underlying fundamentals of Twitter as a public company.

Consumer cyclical remains the second most undervalued sector, trading at a 16% discount to fair value. With the economy weakening in the first half of the year, this sector had been the worst-performing part of the market during that time. We think the best opportunities are in those areas that stand to gain from a normalisation of consumer behaviour. We expect spending will continue to shift back into services toward prepandemic levels and away from goods, which had outperformed during the pandemic. For a more in-depth discussion of these opportunities, please see Spending Is Shifting Back to Services; Here’s Where to Invest Now.

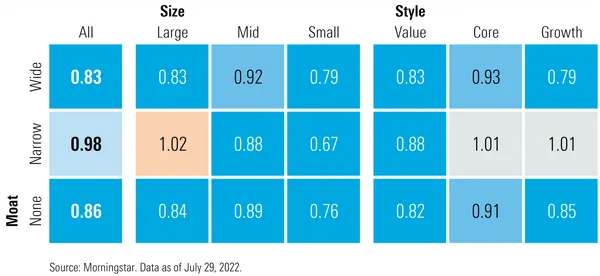

Indiscriminate Selling Puts Wide-Moaters at a Discount

During the worst of the selloff we noted that in order to meet redemptions many portfolio managers resorted to selling what they could as opposed to what they wanted. Stocks of high-quality companies will typically have a deeper pool of liquidity to sell into than lower-quality names.

As a result of this indiscriminate selling, stocks with wide economic moats are trading at a greater discount than stocks of companies with either narrow or no moat ratings.

We continue to see a significant amount of value for long-term investors in wide-moat stocks. In addition to their lower valuations, we also expect these companies generally to have greater pricing power. As such, they should be able to pass through any cost increases to clients and be able to better maintain their margins, and thus sustain their valuations in an inflationary environment.

Our Outlook

We continue to view the broad U.S. equity market as materially undervalued. However, even at the current level, long-term investors should brace themselves and expect volatility to continue over the next several months.

In our 2022 outlook, we noted that there were several headwinds the market was going to have to contend with this year. The two that the market will now most closely be watching for are an economic recovery and moderating inflation. Over the next few months, markets will be looking for signs that these challenges are beginning to abate. Any metrics that indicate the economy is continuing to weaken or that inflation will remain hotter for longer would most likely put renewed downward pressure on stocks.

Based on our forecasts, we think both of these headwinds should begin to shift into tailwinds. For example, even after accounting for the negative gross domestic product reports in the first and second quarter, we’re still projecting real GDP growth of 2% this year. We think inflation has peaked and should begin to moderate from here on out.

"The June [CPI] report will almost certainly mark the peak in inflation, as food and energy prices are set to fall sharply in next month's report," says Morningstar’s chief U.S. economist Preston Caldwell.

We encourage market participants to stick with plans that balance long-term investment goals with their risk tolerances. These plans should allow for periodic rebalancing to increase equity allocations when valuations decline, but also reduce exposure when valuations become overextended.

Based on our view that the US equity market is undervalued, we think now is not the time to be reducing equity exposures but to be adding to them judiciously, especially in companies with wide economic moats.