With its largest interest-rate increase in 28 years, the Federal Reserve signalled a stepped-up determination to fight inflation, even if it ultimately takes a toll on the economy.

The Fed announced Wednesday that it was lifting the federal funds rate by 0.75 percentage points, the largest interest-rate increase since 1994. This marks an aggressive policy shift, as the Fed previously signalled intentions to raise the rate by a smaller 0.50 percentage points.

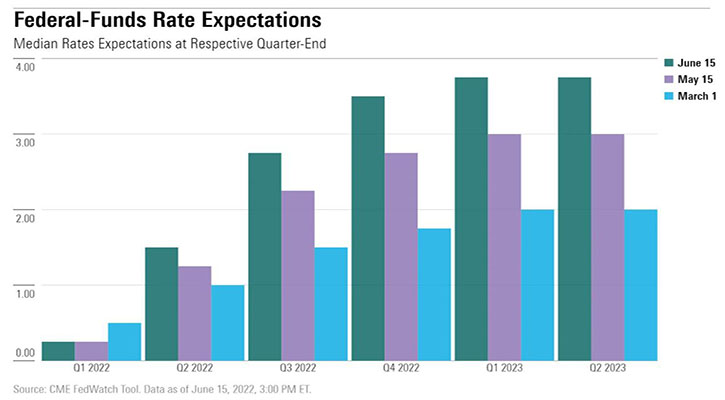

With the latest hike, the federal funds rate rises to 1.5% (the bottom of the target range), up from 0% at the start of the year. Futures markets imply that the federal funds rate will hit 3.75% by the first quarter of 2023, in line with the Fed's official projections.

Fed has signalled a shift to a more hawkish stance, with its determination to bring inflation under control having become increasingly urgent. We think the market is correct in assessing this shift in the Fed's stance.

The two-year US Treasury yield has increased about 0.6% over the past two weeks, with the 10-year US Treasury up about 0.4%. This has added to a sharp rise in bond yields, which began late last year. Because anticipated increases in the federal funds rate are incorporated into bond yields, they are already starting to affect the economy.

With the 30-year mortgage rate now closing in on 6%, housing affordability has suffered immensely. This is bound to have a large negative impact on housing demand and (ultimately) building activity. We had already expected about a 10% drop in housing starts in 2023 prior to the uptick in rates in recent weeks, but now the downturn is likely to be even greater. A downturn in housing will be a major factor in slowing the overall rate of gross domestic product growth.

For now, we don't expect an outright recession, but with our base case incorporating a slower rate of GDP growth, the risk of a recession has become elevated. We project 2.2% real GDP growth in 2023, while the Fed is expecting 1.7%. While the Fed is hoping to avoid a recession as collateral damage in its fight against inflation, it appears comfortable with the risk.

Labour markets are getting closer to a full recovery. The unemployment rate is already essentially back to its pre-pandemic mark, while the overall rate of employment is not far behind as the rate of labour force participation has begun to recover. An economic slowdown would likely cause some temporary deterioration in the labour market, but the Fed's progress in achieving its full-employment mandate is running miles ahead of success in achieving its low-inflation mandate.

Fed chair Jerome Powell mentioned that near-term inflation data had disappointed compared with hopes that signs of progress would begin emerging. The Consumer Price Index increased 8.6% year over year in May. We argued that this stubbornly high inflation increased the likelihood of a 0.75% hike for the Fed meeting in June, which proved correct.

The Federal Reserve's effectiveness in stamping out high inflation depends on how quickly supply shocks — such as the hit to Russian oil supply and the global semiconductor shortage — can resolve. Additionally, if long-run inflation expectations increase and remain high, then actual inflation will remain high even as the Fed achieves a slight slowdown in economic growth. This scenario would require even more aggressive moves from the Fed to reverse the increase in inflation expectations.