The concept of factor investing is a relatively recent concept. It has been closely linked to the appearance (especially in the United States) of exchange traded funds (ETFs) known as strategic beta or smart beta. Although strategic beta ETFs are passive management products, their objective is to beat the return of traditional indexes, or to reduce the risk of the indices, through the use of factors.

Although it may seem like a "new" concept, the foundations on which factor investing is based have been known for quite some time in academia.

Sources of Returns

But what do we mean by factor investing? Factor investing is investing by isolating as far as possible one or several sources of returns. (I say several because the latest in factor investing is multifactor investing or investing according to several factors). What are these sources of return? The academic world is pretty much in agreement in identifying six sources or ‘factors’ of return: value, momentum, size, volatility, quality and dividends.

In the same way that one can invest on the basis of specific regions, countries or sectors, managers can also invest in fundamentally cheap companies (value), in companies that show better relative short-term performance (momentum), in companies with low market capitalisation (size), in companies with low volatility or in companies with high dividend yields.

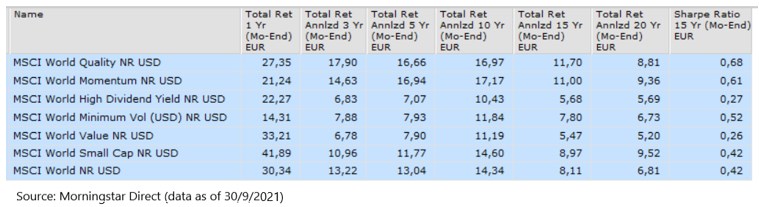

What results have these factors achieved over time? As the attached table shows, it depends very much on the period one looks at and whether one takes risk into account.

How to Identify Factors?

In 1992, Morningstar introduced the Style Box as a way of classifying equity funds according to the size and investment style of their holdings. Since this style box was introduced, we have made progress in our understanding of the different factors that explain equity returns.

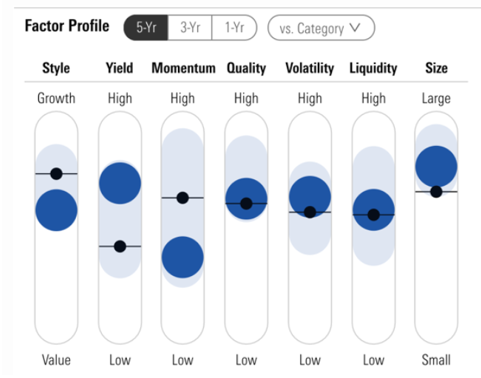

While size and value/growth style exposure can help explain the difference between funds' long-term returns, it doesn’t tell the whole story. Morningstar's Factor Profile is a new tool that complements the Style Box, incorporating additional factors that further explain funds' exposure to well-documented sources of long-term returns.

Morningstar's Factor Profile provides a snapshot of a fund's exposure to seven different factors (the six previously mentioned factors, and liquidity). These factors are common characteristics of stocks that can help explain their long-term returns relative to the market. Each of these factors has been well documented and researched in academia and applied by investment professionals.

How Can Investors Use the Factor Profile?

Investors can use the Morningstar Factor Profile to better understand the different sources of return that equity funds provide and to assess how effectively they are exposed to them.

When considering a fund in isolation, the Factor Profile can be used as a control tool. Do the fund's factor exposures match the way the manager describes its investment approach? Is a strategic beta fund capturing the factor it is aiming to achieve?

The Factor Profile can also be even more useful in comparing similar funds.

Ultimately, there is much more to equity investing than the simple distinction between value and growth.