In investing it's often said that greater risk comes with greater potential rewards - but is that always the case?

Adventurous funds typically have a greater proportion of their portfolio in stocks and shares, while a cautious option may hold more cash and bonds. But a more conservative allocation has done nothing to harm returns in recent years, according to Morningstar data.

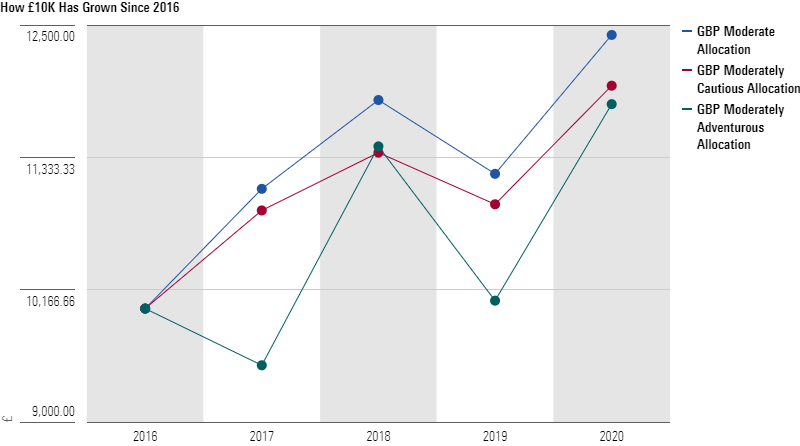

We have compared the performance of three Morningstar Categories - GBP Moderate Allocation, GBP Moderately Cautious Allocation, and GBP Moderately Adventurous Allocation - from January 2016 to October 2020 to see how funds fared.

Funds in each of these categories invest across the three major asset classes (stocks, bonds and cash), but the split is quite different. While an adventurous allocation fund has to invest typically 70% to 90% of its assets in equities, the moderate and cautious allocation funds can invest way less, at 50-70% and 20-50% respectively.

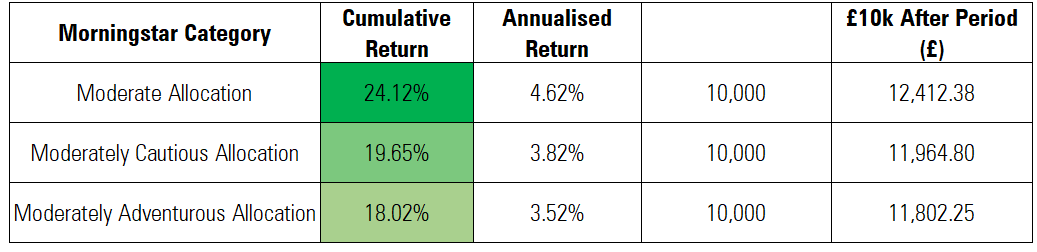

A look at the figures shows that you'd be wrong to assume that ramping up the risk always reaps rewards. The average performance in the Moderately Adventurous Allocation category is actually the weakest over the period, with a cumulative return of 18%. The Moder- which should do better - is, actually, at the bottom. Indeed, it has produced a 18% cumulative return since 2016, while the Moderate Allocation and Cautious Allocation are, on average, 6.1 and 4.5 percentage points ahead of it.

Source: Morningstar Direct data, January 1, 2016 to October 20, 2020. Final value of £10,000 invested January 1, 2016.

Let’s translate this performance into pounds and pence. If you invested £10,000 in a Moderate Allocation fund on January 1, 2016, you would have enjoyed gains some £610 greater than if you'd have chosen the average Moderately Adventurous Allocation fund.

“Over the long-term, you would expect a portfolio with a strong equity weighting to deliver greater returns on average, but what we see here is that the period included a sharp drawdown across all the equities markets due to the coronavirus crisis,” explains Jason Hollands, managing director at Tilney Investment Management.

The Covid-19 induced sell-off of March 2020 was the sharpest move to a bear market on record, says Hollands, so it stands to reason that portfolios with a large equity exposure would be most vulnerable. He adds: “Meanwhile, bonds have done better this year and have been more stable during the crisis as buying programs from central banks in the UK and the US have boosted the value of bonds.”

Indeed, cautious investors have poured billions into the asset class in recent months, pushing bond prices up to new highs. In September alone, the asset class attracted over £1.1 billion of net inflows into both active and passive vehicles, the fifth consecutive month of inflows.

Bad time for the UK market

A troubled time on the UK stock market has also held back performance across these categories. Share prices on the FTSE have battled poor sentiment since the Brexit vote of 2016 and the volatility of a General Election and global pandemic have only exacerbated the situation. This year has seen a raft of UK firms slash dividends, with research showing that 2020 has been the worst year for income investors since 2009.

Despite the volatility, however, Mark Preskett, portfolio manager at Morningstar Investment Management, says the performance figures are surprising. Over the long-term investors would typically expect equities to outperform, and for aggressive allocations to outperform cautious portfolios.

He adds: "The underperformance is all about the weakness of the FTSE and UK Equities over the last few years. If you look at the FTSE All Share’s performance over the last five years, it's right at the bottom of the pile, and way behind regions such as the US and Japan.”

In an environment where UK equities underperform and bonds thrive, cautious funds tend to do better. “You get this strange situation of aggressive funds underperforming lower risk profiles,” says Preskett.

But, as the common investment adage goes: past performance is no guarantee of the future, and Preskett doesn't expect this trend to continue. Clarity over Brexit could provide a welcome tonic to the UK stock market, so it's may not be time to hit the sell button just yet.

Preskett adds: “Ultimately, equities do deliver good long-term returns for investors and the level of outperformance of UK bonds over UK equities that we have seen is unlikely to persist over the next five years."