So far 2020 has been a year of winners and losers. Whether it's tech soaring while energy stocks struggle, or the US stock market trouncing emerging markets. And this disparity is evident even among the top-rated funds.

Investors have poured around £2.5 billion into funds rated Gold by Morningstar analysts this year, and £4.5 billion over 12 months. That’s not surprising given these funds have proved their mettle during the worst of this year’s crisis. But not all of the Gold-rated cohort have proved so popular; a number have bled hundreds of millions of pounds in assets as nervous investors have taken their money elsewhere.

Of the 24 funds rated as Gold for which Morningstar has up-to-date flows data, 15 have seen positive inflows for the year. Changes to Morningstar's ratings framework, which puts an enhanced focus on fees, means it's harder than ever for funds to achieve the coveted Gold rating - that been highlighted by the downgrade of the popular Scottish Mortgage Investment Trust (SMT), which was recently downgraded to Silver even after delivering returns of 70% in a year.

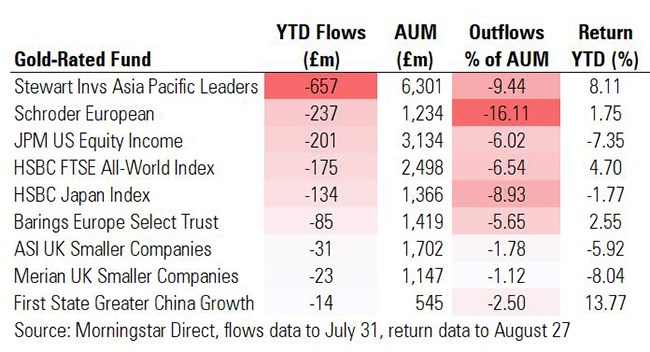

Among Gold-rated funds, Vanguard FTSE UK All Share Index brought in £1.59 billion of new money in the year to date. But at the other end of the spectrum, nine Gold-rated funds have experienced net outflows this year. Chief among them is Stewart Investors Asia Pacific Leaders, which has suffered net outflows of £657 million year to date. It is followed by Schroder European, which bled £237 million in assets.

Of course, outflow numbers alone don’t tell the full story. We've looked at each fund's total assets under management across all share classes to see what percentage of assets each has bled this year.

On this basis, Stewart Investors Asia Pacific Leaders also leads the pack, with a chunky £6.3 billion of assets under management. It has suffered as some of the countries it invests in, such as India, are currently out of favour with global investors. Indeed, a look at the performance of the funds in this cohort indicates that these outflows are likely being driven by sentiment rather than returns - indeed, many are in positive territory year to date.

Here we look at some of these funds, what they invest in, how the've performed and what Morningstar analysts think of the managers:

Stewart Investors Asia Pacific Leaders

Managed by David Gait and Sashi Reddy since 2016, Stewart Investors Asia Pacific Leaders was upgraded by Morningstar analysts to Gold in February 2020. “We believe the group to be among the best Asian equity investment teams,” says analyst Andrew Daniels, who praises the “robust and differentiated investment approach”.

Year to date the fund has posted gains of 8%, comfortably ahead of the average 6% gain for the Asia-Pacific ex-Japan category. Over longer time periods the fund’s performance has been more impressive, with a 10% annualised gain over 10 years – significantly outperforming the MSCI Asia-Pacific ex-Japan equity index. “There are many reasons to believe that such strong returns will continue,” Daniels adds.

The fund is skewed towards emerging Asia, which accounts for 46% of the portfolio, while developed Asia makes up around 26%. Japan is the next biggest component with an 18% allocation. Japanese nappy and pet care firm Unicharm (8113), is the fund’s top holding, followed by another Tokyo-listed company, optical expert Hoya (7741).

First State Greater China Growth Fund

The Gold-rated fund with the smallest outflows in absolute terms also has an Asia-Pacific focus. First State Greater China Growth Fund, which has seen a marginal net outflow of £14 million year to date, is also the smallest by assets under management amon this group with £545 million of investor money in the fund.

China funds have been some of the best performers in 2020 as the country went into and subsequently emerged from lockdown much faster than others. This fund is up 13% this year, but this is behind some of the best-performing China funds: according to Morningstar Direct data, its rival Schroder China has posted gains of 35% this year, as has JPM China A-Share Opportunities. Indeed, the average return in the Morningstar Greater China category is 18% year to date.

Morningstar analyst Germaine Share says the First State fund is “backed by a talented manager, strong investment team, and a time-tested investment process”. She describes manager Martin Lau as an expert investor with a “tried and tested bottom-up stock selection process, which looks for quality growth companies”. The portfolio is relatively concentrated with around 60 companies and the manager has a particular focus on stocks with strong corporate governance, she adds.

Taiwan Semiconductor (2330), a favourite of emerging market investors, is the top holding in the First State fund with a 7.6% weighting, followed by just over 7% in Tencent (00700).

Merian UK Smaller Companies

Another fund where outflows this year have been more of a trickle than a flood is Merian UK Smaller Companies. The UK remains out of favour for obvious reasons, including Brexit and coronavirus, which has hit smaller and medium-sized companies harder than multinational stocks. Many of these firms are directly exposed to the UK economy, which contracted by 20% in the three months to June, the worst performance of any G7 nation.

The Merian fund has fallen 8% in 2020 but its longer-term performance is much more impressive, with 10 year annualised gains of 14%. For comparison, the average Morningstar UK Small-Cap Equity category fund is down 11% in 2020. Performance this year has been held back by a share price slump in its top holding, Aim-listed fashion firm Boohoo (BOO), which is under fire for working conditions at its factories. In contrast, shares in its second biggest holding, Liontrust Asset Management (LIO), has risen nearly 70% over one year.

Morningstar analyst Samuel Meakin continues to rate both the fund's manager and stock selection process highly: “Merian UK Smaller Companies continues to represent a very strong option in the UK small-cap space, benefiting from a long-tenured manager skilfully executing a consistent approach with the support of a well-regarded team.”

He adds: "The team aims to find companies with the ability to grow earnings faster than the market average for an extended period of time, the scope to generate a positive surprise, or the potential to be rerated relative to the market.”