The UK regulator has been on a drive to bring down fund fees for many years now. The Retail Distribution Review of 2013, the FCA study of fund fees, and last year's introduction of Value Assessment Reports are putting the fees companies are charging people to invest front and centre. The big question: is it working?

We analysed fees on both active and passive UK equity funds since 2012 to see what is happening. Morningstar Direct data shows that over an eight-year period, charges are trending downwards.

Our sample looks at the annual report ongoing going charge of 1,474 UK-domiciled UK equity funds across five Morningstar categories: UK Equity Income, UK Flex-Cap, UK Large-Cap, UK Mid-Cap and UK Small-Cap. We’ve excluded active funds and passive trackers whose ongoing charge was less than 0.19% and 0.05% respectively, which typically reflects fees that have been negotiated for big institutional investors.

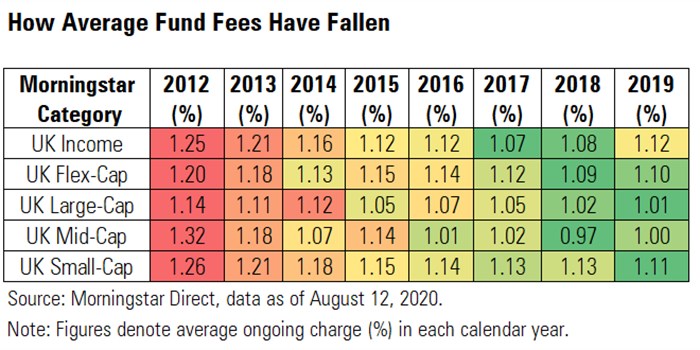

Fund Fees are Falling

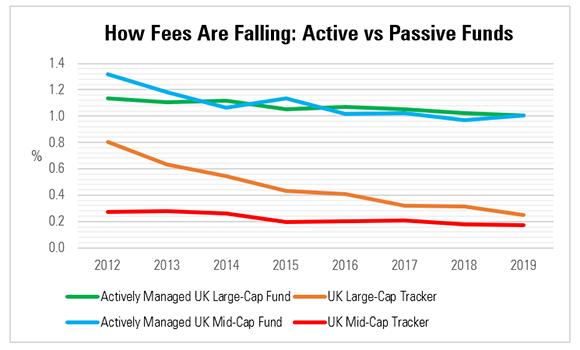

According to our analysis, the average fee for active funds across the categories reviewed has fallen by 13% since 2013. Eight years ago the average fee on active funds in these groups was 1.23% and today that has dropped to 1.07%.

One of the key drivers of this trend is the growing use of cheap tracker funds, says Teodor Dilov, fund analyst at interactive investor. With newer passive funds charging as little as 0.06% in some instances, active fund managers have had to cut costs too. "Considering only a minority of fund managers beat the market over a full market cycle, it is natural to review and reduce the fees for products that do not deliver," says Dilov.

After all, why would an investor pay 1% for an actively managed fund that invests in UK large-caps, when they could own a FTSE tracker fund for a fraction of the cost?

Some of the biggest savings for investors can be seen in the UK mid-cap equity category, where fees have fallen by almost a quarter since 2012, from 1.32% to 1%. “The mid-cap seems to stand out in terms of being a slow-starter but a bigger reduction over time”, says Andy Pettit, Morningstar's director of policy research.

The savings across active UK small- and large-cap funds are smaller, with fees falling by 12% and 11% respectively over the period. The UK Equity Income category has the highest average fee, both in 2012 (1.23%) and today (1.1%).

But not all investors are enjoying these falling fees; there remains a great disparity between the most expensive and the cheapest funds in each group. The most expensive fund in our sample within the UK large-cap category, for example, is Schroder MM UK Growth A, with an ongoing charge of 1.8%. This compares with the cheapest fund in the group, JPM UK Equity Core E, which charges 0.31% - almost a sixth of the price. Multi-manager funds, also known as fund-of-funds, are typically more expensive, it is worth noting.

There are also still great difference between the various share classes available to investors and Alan Miller, founding partner at SCM Direct, points out that investors should do their research also when it comes down to a singular fund. Indeed, the BMO UK Smaller Companies 3 fund, for example, charges just 0.22%, while another of its share classes, BMO UK Smaller Companies 1, has an annual charge of 1.77%.

Passive Options

Passive funds, also known as tracker funds, have surged in popularity in recent years. Investors are often attracted to the low price and simplicity of these investment products. And while older, open-ended index funds have historically charged a similar fee to actively managed funds but the rise of exchange-traded funds (ETFs) has ramped up the pressure to change.

As a result, fees across passive funds have also fallen significantly since 2012, and often to a greater extent than with their active counterparts. The average fee for passive UK large-caps, for example, has dropped by 69% over eight years. The average charge has fallen from 0.8% to 0.23% across the group. Among UK mid-cap trackers, the average charge has dropped from 0.28% in 2012 to 0.15% today.

Alan Miller, founding partner at SCM Direct, says: “Tracker funds used to charge very high fees, but as price competition has increased, they have been forced to lower their charges.”

The upward march of investment giants such as Vanguard and Blackrock has sparked something of a price war among tracker funds in recent years, with investors realising there is no need to pay over the odds to track an index. Silver-rated funds HSBC FTSE All Share Index and Fidelity Index UK fund charge as little as 0.06%.

What's Driving the Charge Change?

The Retail Distribution Review (RDR), which came into effect in 2013, has undeniably influenced the market and fund fees. One of its main goals was to stop fund companies from paying trail commission to advisers and platforms. The removal of commission led to a flood of new so-called "clean" share classes being created.

“This moved the industry from a commission to fee-based model, aiming to align the advisers interests with their clients',” says Dilov. “In addition, transparency requirements lead to stronger focus further pressure on fees for all participants in the chain.”

Consolidation within the investment industry has also been a factor, creating larger companies that are able to pass on the economies of scale to investors. Furthermore, another milestone was reached last year when the FCA introduced a new piece of regulation in the form of Value Assessment Reports, forcing funds to analyse whether they are providing value of money to investors. This month, for example, Jupiter published its first batch of reports, concluding that only 64 of its 91 share classes are delivering value for money.

Pettit believes the rules put a strong onus on fund boards to consider their fund offerings from the perspective of their investors. “We are seeing a sunsetting of many of the remaining legacy clean classes and selective fee reductions on individual funds as they are assessed relative to similar mandates, competitor offerings and economies of scale,” he says.

But while much has been done to lower fees, commentators say there is still a long way to go. “Greater onus has been placed by regulators on asset managers to show that they are indeed providing value for money for customers," says Dilov. "The fall in fund ownership is a good start, but there’s a feeling that asset managers can do more to this end.”