It’s not often that investors can feel heartened to see their investments have fallen in value, but looking at the big picture is crucial in a market sell-off. At a time when it has been almost impossible for fund managers to generate a positive return, looking at how they have fared against their rivals and to the wider market is key.

A look at the equity funds with a track record of at least 10 years shows that judging performance on one month alone only tells part of the story. Funds are grouped into categories based on their investment remit, those which focus on UK Smaller Companies, for example, or on equities in a broader region such as Europe or Emerging Markets. A fund’s performance relative to its whole category indicates the strength of its investment process, even during times of turmoil.

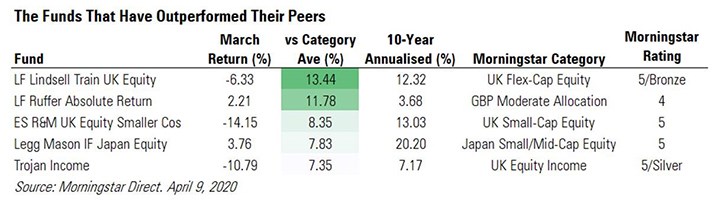

We have looked at the performance of funds in March 2020 when the FTSE 100 plunged by more than 25%, the oil price collapsed and countries the world over went into lockdown. While the numbers don’t make for easy reading, we have then compared it to the average performance achieved by funds in their Morningstar Category to find those that have outperformed (or underperformed) their peers.

Lindsell Train UK Equity tops the table; while the fund was down 6.33% in March, it outperformed the UK Flex-Cap Equity category by an impressive 13.44% percentage points. That means the average fund in the sector was down an eye-watering 19.77% in the month.

Fund manager Nick Train is known for his buy and hold approach to investing, rarely adding new names to his investment portfolio, and he favours quality consumer companies with a loyal customer base with big stakes in Guinness-maker Diageo (DGE) and chocolate giant Mondelez (MDLZ).

The benefits of owning this type of company is that they should continue to do well regardless of an economic downturn, as shoppers typically still spend on chocolate and alcohol through recessions; the same can be said for the fund’s top holding Unilever (ULVR), which is behind big household favourite brands such as Dove, PG Tips and Domestos. As well as outperforming during the recent volatility, the fund has delivered annualised returns of 12.32% over the past 10 years.

Investors might be surprised to see an Absolute Return fund second on the list of top performers; these funds have been out of favour in recent years as many have not achieved their target of delivering a positive return. Absolute Return funds often have a cautious objective to deliver a return that beats inflation or interest rates, so can seem less appealing when stock markets are soaring as they have over the past decade. However, the benefits of owning funds with more modest aims come to fore at times of uncertainty. While

Ruffer Absolute Return has delivered annualised returns of just 3.68% over the past decade and it was one of just a handful of funds in positive territory in March. Up 2.21% for the month, it outperformed its peers by a hefty 11.78 percentage points.

Legg Mason IF Japan Equity has the greatest 10-year annualised returns among the top flight, at 20.2%. It also outpaced its category by 7.83 percentage points in March, delivering a positive return of 3.76% for the month.

Value Funds Underperform

At the other end of the spectrum are the funds that have underperformed their Morningstar Category. JOHCM UK Equity Income was down 25.3% in March, some 7.17 percentage points lower than its rivals. The Silver-Rated fund has been hurt by its exposure to banks, which were forced to suspend their dividend payments, and oil giants such as BP and Shell, another sector which has had its ability to pay dividends cast into doubt as the oil price has fallen below $30 a barrel.

Morningstar analyst Peter Brunt admits the fund’s strategy of avoiding “en vogue” investment areas can leads to periods of weakness, but says: “We continue to have a high level of conviction in the fund’s ability to outperform over the long-term, while providing an above-average yield and growing income stream.”

With a focus on unloved UK stocks, the Dimensional UK Value fund has also struggled to keep up with its peers in the sell-off. Down 22.62% in March, it has underperformed the UK Large-Cap Equity category by 6.55 percentage points as investors have favoured quality, defensive stocks over cyclical, value ones. Indeed, the fund’s top holdings include banking giants HSBC (HSBA) and Lloyds (LLOY); the sector is firmly in the spotlight in the coronavirus pandemic as banks issue loans to struggling businesses and offer worried customers holidays on mortgage and credit card repayments.