More than three-quarters of British employees are now members of a workplace pension scheme, according to new figures from the Office for National Statistics. And for the first time, occupational defined contribution (DC) pensions have overtaken all other types of pension, including defined benefit (DB) or final salary schemes.

The proportion of employees in a workplace pension hit 77%, the highest since comparable records began in 1997 – it marks a huge advance on the 47% in these schemes when auto-enrolment started in 2012. At the time pensions minister Steve Webb, said: "Few policies affect as many people, and this will be a truly radical social change.”

And for the first time, in public sector schemes at least, there is no gender savings gap. In private sector schemes, however, women lag men in pension take-up: 77% of men are signed up to company pension schemes, against 69% of women.

With the decline of final salary pension schemes, auto-enrolment was designed to widen the net of pension savers – instead of having to opt in, employees were automatically signed up and would have to actively choose to drop out.

The minimum contributions in auto-enrolment have increased since the reforms came in – in the latest tax year, 2019-2020, the minimum contribution is 8% of a worker’s salary (up from 5% the year before), and that is made up of employer and employee contributions, as well as tax relief from the Government. Encouragingly, as contribution rates have gone up, the drop-out rate has not risen.

AJ Bell analyst Tom Selby said: “The fact there are now more defined contribution scheme members than defined benefit is testimony both to the success of auto-enrolment and the continuing demise of guaranteed pensions in the private sector. While many will lament the slow death of DB, DC is the future of retirement saving in the UK and the focus needs to be on making this avenue as attractive as possible for savers.”

Will 18-Year Olds be Auto-Enrolled?

Auto-enrolment applies to workers age 22 years old and over, who are earning at least £10,000 a year. Companies that employ more than one person have legal obligations to put people an employee in a pension scheme. The Pensions Regulator says more than 10 million people are now enrolled in workplace pensions, with 1.4 million companies taking part.

The Government is considering lowering the age of auto-enrolment and changing the “qualifying earnings” band to widen the net further, but there is no timescale for these changes. Since 2012, the rate of participation among those between 22 and 29 has rocketed from 31% to 80% last year.

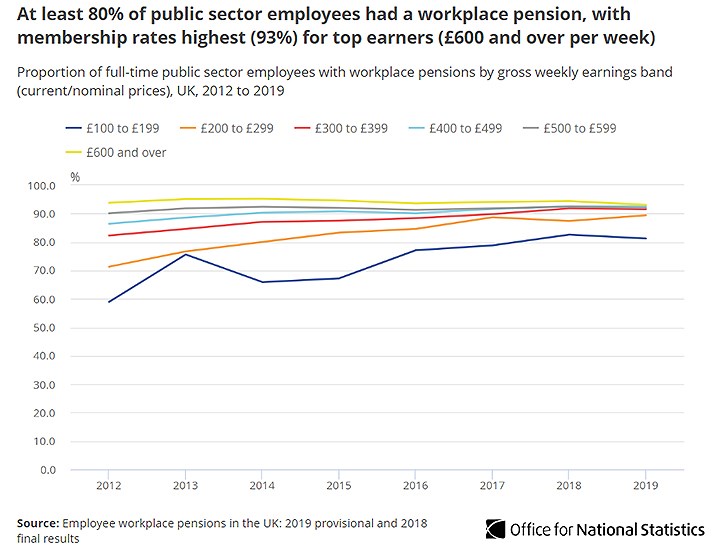

Public sector workers are more likely to be members of an occupational pension scheme, the ONS says, with at least 80% signed up. Within this group, 93% of those in higher income brackets (earning £600 and over a week) were signed up, compared with just over 80% for those earning £100-£199 a week. While the level of higher earners in public sector schemes has remained constant above 90% since 2012, there has been strong growth in the take-up among lower earners, from just under 60% seven years ago to above 80% last year.

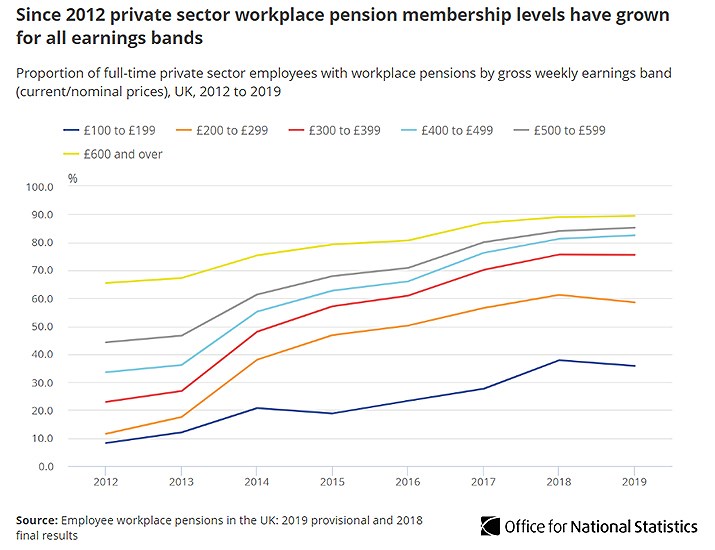

The profile of private sector employees is similar at the top end to those in the public sector, with around 90% of the highest earners signed up. But that drops to just above 35% for the lowest earners in company pension schemes (this was below 10% in 2012). In the public sector, nearly all but the lowest earners are signed up to a pension, with most earnings bands around 90% enrolled.

But just under 60% of those private sector workers earning £200-£299 a week are signed up to their company pension – only 10% of these workers were signed up in 2012, suggesting auto-enrolment has had the biggest impact among lower income brackets, especially with many of these people just starting out in their working lives.