When BlackRock chief executive Larry Fink unveiled his new vision for sustainability as the "new standard for investing" last week he charted an ambitious course for his firm and its investors, and threw down the gauntlet to BlackRock's competitors.

Fink highlighted the hurdles that environment, social and governance (ESG) investing needs to overcome to make it into a mainstream investment strategy with broad acceptance among investors and the financial-services industry. These are also challenges that BlackRock itself must show it can meet.

Fink's argument is that climate change is a real risk throughout the global economic landscape; sustainable investors should incorporate this risk into investment decisions and portfolio construction.

This notion of ESG as an investment risk is at the heart of the updated Morningstar Sustainability Rating language. The sustainability rating is now based on assessments made by our partner, Sustainalytics, as to individual companies managing the ESG risks particular to their industry and business.

Fink's belief that fund companies and investors have a role to play in managing and alleviating the climate risks we face means that sustainable investing has to be more than just "greenwashing", using ESG as an asset-gathering and marketing ploy. A true ESG mandate comes with a set of responsibilities that requires fund companies to relinquish their traditional posture of neutral middlemen.

More Choice

Recently investors have been flooding money into broad-based indices, and target-date funds have become useful for retirement. For ESG investing to become more widespread, it will need to ride those waves, not fight them. Flows into sustainable funds, while hitting new records each year, are still tiny compared with the billions poured into passive options like index trackers and ETFs.

Part of the problem is that many ESG-focused funds don’t have track records of more than three years, and assets under management are small. Of course, time will lengthen track records of new funds. But the overall number of investment choices remains slim.

In terms of BlackRock's ESG lineup, Fink addressed this from a global perspective, saying the firm would double the number of exchange-traded funds and index funds to 150: out of iShares' current ETF lineup of roughly 370 funds, 14 are ESG strategies.

In addition, Fink said BlackRock would develop a sustainable LifePath target-date strategy and work to build adoption of ESG strategies among retirement plans.

Cost is a Barrier

The dramatic shift among investors toward index strategies isn't just a story about the kinds of funds they invest in, it's how much they cost. Investors are not just moving to lower-cost funds, they are choosing the cheapest available options.

ESG investing was traditionally the domain of smaller, specialised asset managers, and their higher fees reflected that niche aspect of the group. That left investors facing a question: how much more am I willing to pay to save the earth?

There remain more opportunities to make ESG investing more competitive. In many fund categories, there's a scarcity of low-cost ESG funds.

Of course, it's not a surprise that a fund with an added layer to the investment process – in this case an ESG screen – will cost more than a market-cap-weighted index. But how much additional cost is really required? Narrowing these expense ratio gaps will be crucial to ESG's acceptance.

Voting Matters

There are few levers that funds can pull in order to have an impact on the companies whose stocks they hold: they can lobby management, vote in corporate elections (proxy voting), or sell the stock. Index funds are locked into holding stocks contained in the index they are tracking.

Fink now says BlackRock "will be increasingly disposed" to vote against company managements that hasn’t made enough progress on sustainability issues. He also took a step that would propel the firm into a leadership position: BlackRock will start reporting proxy votes on a quarterly basis, and on certain high-profile votes, it will immediately disclose its votes along with an explanation.

There are several ways for BlackRock and other fund companies to have a real impact: they need consistent votes in support of issues, to vote down directors showing poor oversight of environmental and sustainable issues, and to vote down “say-on-pay” resolutions where sustainability metrics aren't part of the determination.

Active Interest

How will a large, established firm like BlackRock fully integrates ESG into its existing strategies?

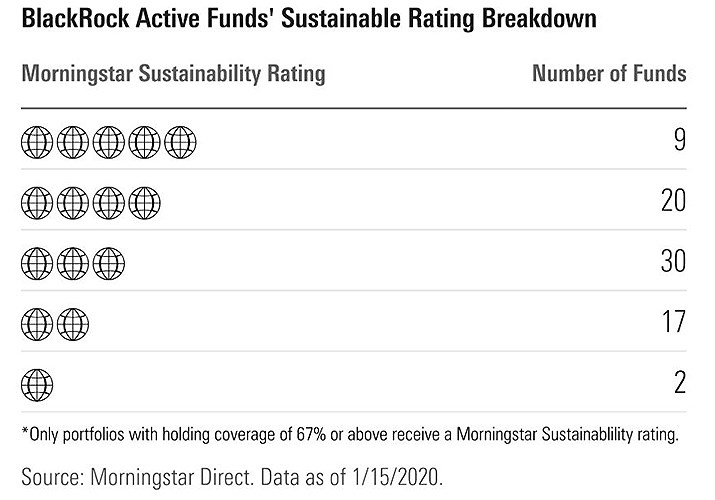

One measure to watch will be the sustainability ratings on BlackRock's actively managed funds for signs of improvement. Out of the 78 active funds that receive sustainability scores, nine receive the highest rating of 5 globes, and 20 have above-average ratings with 4 globes.

For active managers broadly, it may be that they see ESG as a new opportunity to beat the market, especially in parts of the stock market where they have had a harder time differentiating themselves, such as large-cap stocks. For investors, however, this creates some confusion and uncertainty. When ESG is just one factor in a fund's process, investors can't rely on that fund profile remaining the same.

Morningstar's own metrics are evolving to factor in the explosion funds which aren't offered as ESG products per se but incorporate "ESG considerations" into their investment strategies. Starting on January 31, Morningstar's labelling of a fund as an ESG fund will be limited to those strategies that employ ESG as a core part of their process.

BlackRock's Fink has charted an ambitious path for ESG investing to become accessible and accepted. The next step would be for BlackRock and other firms to follow through on taking that path.

:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/6BCTH5O2DVGYHBA4UDPCFNXA7M.png)