When it comes to finding the funds that can deliver the best long-term returns, it pays to check who the manager is and, crucially, how long they have been at the helm.

Morningstar analysis shows that often the longer a manager has run a fund, the more likely it is to outperform.

James Henderson, for example, is the longest-serving manager on a UK Equity Income trust. He has run the Silver-Rated Lowland Investment Company (LWI) for 30 years. Over the past 10 years, his trust has delivered annualised returns of 12.2% compared to just 8.2% by the benchmark. It is testament to how a long-term view, consistent investment process and established team can reap rewards for investors.

“Investors can benefit from the rich experience that managers have, running portfolios in good times and bad,” says Nick Britton, of trade body the Association of Investment Companies (AIC).

A look at the UK Equity Income sector for both investment trusts and open-ended funds highlights how a manager’s tenure can impact returns:

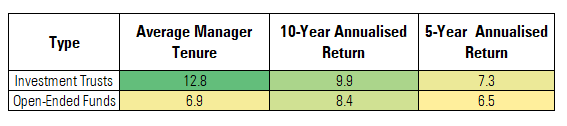

The average manager tenure in the sector among investment trusts is 12 years 10 months, according to Morningstar Direct, while among open-ended funds the average manager has been in place just 6 years 11 months.

And it appears that where managers have in place longer, their performance tends to benefit. Over 10-years the average annualised return of UK Equity Income investment trusts is 9.9%, compared to 8.4% for open-ended funds. The same is true over a shorter time frame: annualised returns over five years are 7.3% and 6.5% respectively.

Of course, there are other factors at play that have helped investment trusts to greater returns over the past decade. Trusts can use gearing (borrowing) which can magnify returns in a bull run, such as investors have enjoyed over the past ten years or so, and they can also keep aside some of their gains to make up any shortfall in leaner years. But manager tenure must also be a factor.

Long-Standing Managers

Close behind Lowland’s Henderson for the title of longest tenure is Job Curtis, manager of the Silver-rated City of London trust (CTY). The manager has run the trust – which has raised its dividend for an incredible 52 years in a row – since 1991. Under his watch, it has delivered annualised returns of 10.8% over the past decade. Morningstar analysts praise the consistency of Curtis’s process as a “prudent and measured approach [that] has resulted in outperformance over most time frames”.

Chelverton UK Dividend Trust (SDV) has produced the strongest long-term returns of the trusts with the longest-standing managers. Headed up by David Horner since 1990, the five-star rated trust has delivered annualised returns of 16% over 10 years.

Experts point out that the better a manager does, the more likely they are to remain at their post too, creating something of a self-fulfilling prophecy. Darius McDermott, managing director at Chelsea Financial Services, explains: “There will be an element of survivorship bias here – if a manager is good, they have longevity. Any managers who have underperformed for any length of time tend to get moved or let go.”

Of course, the hypothesis does not always hold true. British & American (BAF), for example, has underperformed the sector average in terms of its 10-year annualised returns, despite having had the same manager for 24 years. BMO Capital & Income (BCI) has also underperformed the sector average, although it has delivered greater annualised returns than its benchmark over three, five and 10 years.

It is not just closed-end funds that manage to keep their managers for an impressive period of time either. Francis Brooke has managed the Trojan Income fund for more than 15 years, while James Lowen and Clive Beagles have shared the management of the JOHCM UK Equity Income fund for just as long. The funds, both Silver-Rated by Morningstar analysts, have both produced stronger annualised returns than their benchmark over three, five and 10 years.

However, only three UK equity income funds have a manager who has been in place for over 10 years, versus 13 trusts, despite there being a similar number of funds in each sector.

Why Does Tenure Matter?

Managers who have run the same fund for a long period of time are more embedded within the investment team, know the fund and the companies it invests in better, are familiar with their analysts and know how to use the resources at their firm, which can vary dramatically between investment houses.

A manager’s tenure is a key factor for many investors, including Morningstar analysts, who consider it as part of the “people pillar” in the assessment criteria used to assign Morningstar Analyst Ratings - Gold through to Negative.

“We want to see repeatability, and one of the clearest indicators is how disciplined an investor has been in implementing their approach in the past,” says Morningstar associate director Peter Brunt. “The longer we have seen an investor execute their approach in a way that we would expect, the greater confidence we can have that they will keep this course in the future.”

For example, he likes that JOHCM’s Lowen and Beagle have worked together for more than 15 years as it means they understand each other’s skills. “Beagles' strength is in identifying macroeconomic trends, while Lowen complements him with his astute bottom-up analysis,” Brunt adds.

So important is tenure that when a manager moves from a fund rated by Morningstar analysts, it will immediately be placed under review. Recent examples of this include Schroder Tokyo, which was downgraded to Neutral from Gold last year, after its manager Andrew Rose retired and was replaced by Masaki Taketsume.

Succession planning can help to offset such a downgrade but while a manager can claim he will run the strategy in the same way, analysts need to see the evidence. “We like to see managers who have been running the same strategy for at least one market cycle, as we can then make an assessment on how they fared in both bull and bear market conditions. As our current cycle continues to extend, it is harder to build the same level of conviction in those who have become managers only since the financial crisis, which was our last bear market,” explains Brunt.

Meanwhile, the Jupiter European fund was downgraded to Neutral from Gold last year when manager Alexander Darwall left the firm to set up his own outfit. Interestingly, his Jupiter European Opportunities Trust he runs was only downgraded one rung from Gold to Silver because the board of the trust decided to keep him on as manager despite him leaving Jupiter. The trust has since been renamed European Opportunities Trust (JEO).

Brunt, however, notes that manager tenure is just one aspect that investors should take into consideration when assessing a manager. Factors such as alignment with investors, remuneration structure, flexibility and scope for pragmatism in the process and supporting resources available are as just as important, if not more so.