Individual savings accounts (Isas) are an ideal way for investors to build towards their financial goals.

But one of the most important things in choosing where to allocate your money is to determine how much risk you can tolerate. Riskier investments such as stocks have historically shown better potential for long-term growth, but can result in greater losses at times of market volatility such as we have seen in recent weeks.

By the same token, capital preservation-oriented investments such as high-quality government and corporate bonds are better suited to protect during market volatility, but less likely to deliver strong returns over the long-term.

Benefits of a Balanced Portfolio

For the average Isa investor with a moderate risk tolerance, using passive funds to build a balanced portfolio to strike a balance between capital preservation and growth can be a good option.

Dividing assets equally between diversified stock and bond ETFs can protect from unfavourable market movements in the short-term while offering good long-term growth potential.

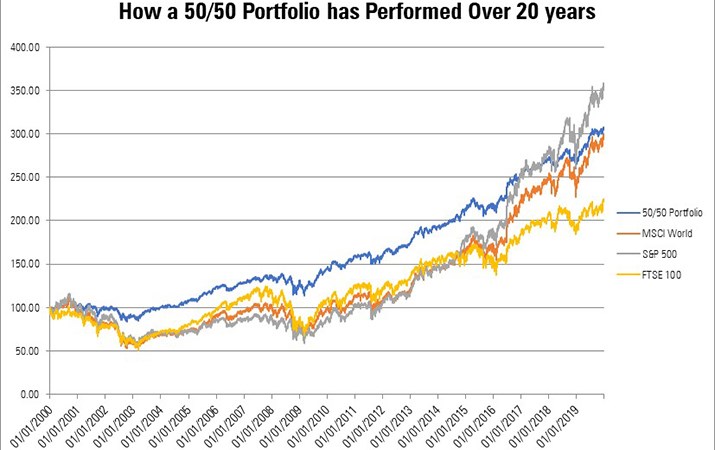

For example, a very simple balanced portfolio split 50/50 between two global stock and bond ETFs has delivered higher returns than key equity market indices such as MSCI World or FTSE 100 over the past two decades.

In fact, as we can see from the below chart, even the phenomenal bull run of the S&P 500 since 2009 would have only placed the US equity index just above the returns delivered by the 50/50 portfolio (see exhibit 1). The real benefit of diversification is to protect on the downside. This was particularly evident during the early 2000s tech crash and the financial crisis in 2008.

Source: Morningstar Direct. 50/50 equity/bond portfolio, Jan 1, 2000 to Jan 31, 2020.

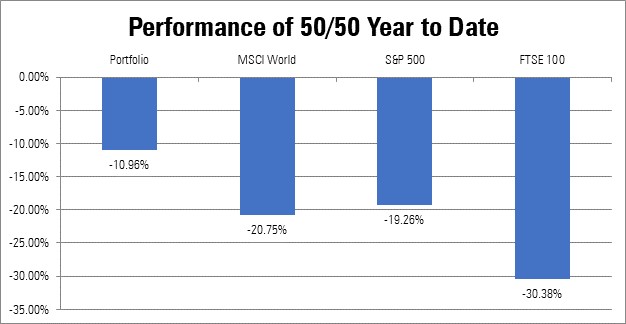

The portfolio’s ability to shelter capital has come to the fore once again during the current market volatility caused by Covid-19. As the FTSE 100 and the S&P 500 have plummeted by around 30% and 15% respectively in a matter of weeks, this balanced investment strategy has limited the fall to just 10% (as the chart below shows), even though quite substantial jitters have been felt in international bond markets too.

Source: Morningstar Direct. 50/50 equity/bond portfolio. an 1, 2020 to March 24, 2020.

How to Build a Portfolio in 3 Steps

Step One: Pick Your Equity ETF

For the equity allocation, investors can consider the Vanguard FTSE Developed World ETF (VEVE) or the Lyxor Core MSCI World (LCWD). These are broad and diversified ETFs that cover nearly every developed country stock. With an ongoing charge of only 0.12%, they are the cheapest among passive peers and certainly very competitive relative to the average active fund in the category.

Currently, the US accounts for 60% to 65% of the index value, followed by Japan (8-10%), the UK (5-7%), and France (3-5%). They also offer balanced sector exposure. As of this review, financial services and technology represent 15-20%, followed by healthcare 10-15% and industrials (10%). Portfolio concentration is very limited, with the top 10 holdings accounting for around 15% of the indices value.

Step Two: Pick Your Bond ETF

For the bond allocation, investors can opt for the SPDR Global Aggregate Bond ETF (SPFB) or iShares Core Global Aggregate Bond UCITS ETF (AGBP). Both track the same Bloomberg Barclays Global Aggregate Bond Index and come with an ongoing charge of 0.10%.

Holdings include a broad range of investment-grade government, supranational, corporate and securitized bonds from a large number of developed and emerging economies.

Both ETFs also come with the advantage of a hedge to GBP, which can help to mitigate the impact of short-term currency movements.

There are versions of these ETFs hedged to EUR and other currencies (e.g. CHF), as well as also unhedged versions to suit the varying needs of investors in EMEA and their attitudes to foreign exchange risk.

Most holdings are government bonds (55-60%), followed by bonds issued by government-sponsored agencies (10-15%). The remainder is split by the likes of corporate bonds, mortgage-backed securities and local authority bonds.

US issuers accounts for around 40% of the index, with a large presence of US Treasuries. Japan follows with just over 15%. France, Germany and the UK account for around 5% each. The combined weight of emerging market issuers is 10%.

Step Three: Rebalance

Rebalancing the portfolio in order to keep the targeted 50/50 allocation is very important because it helps to control risk. This requires selling investments from the ETF that has outperformed and reinvesting the proceeds into the ETF that has underperformed. Typically, in periods of strong market performance, the weight of the equity ETF will grow larger, while in times of crisis its value will drop.

Failing to rebalance is likely to result in increased risk if the equity allocation’s weight grows, or limited returns if the weight of the bond allocation goes too high. However, rebalancing must not be done too frequently as it will rack up high trading costs; sticking to a simple 10% buffer will likely suffice for most investors. This means that once the weight of the one of the ETFs gets to 60% of assets, they should be brought back to an equal weight.

ETFs are excellent as basic building blocks in a portfolio. This simple balanced portfolio is a solid option for an Isa investor looking for an uncomplicated way of investing for the long-term. With just two ETFs you can capture most of the investable stock and bond market at a very low cost and with a high level of diversification.

Very importantly, ETFs help to keep running costs low. The average ongoing charge of our sample portfolio is just 0.11% per year. However, there will be additional costs to sustain every time you rebalance.