Cash remains the overwhelming popular option for tax-free savers, according to the latest data from HMRC on Individual Savings Accounts (Isas). Cash Isas made up 75% of all new Isa accounts for the tax year 2019/2020, the final month of which included the first month of UK lockdown and the stock market crash. The data also showed that Lifetime Isa accounts, which are designed to help younger people buy their first property, more than doubled in a year.

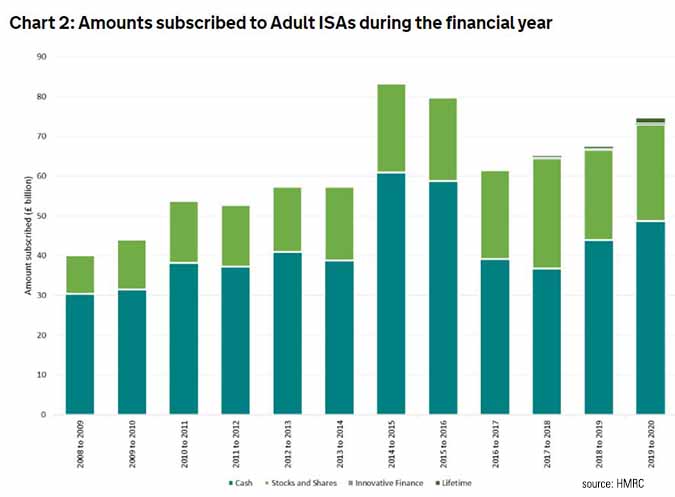

Around 13 million Isas were opened in the tax year 2019/2020, up 16% from 11.2 million in the previous tax year. This is still below levels seen 10 years ago, when 15 million accounts were opened in the 2010-2011 tax year. The amount subscribed in the financial year, £75 billion, was a £7.1 billion increase from the previous tax year and the highest amount since 2015/2016, when nearly £80 billion was saved and invested. Overall, the amount of money subscribed into Isas in total hit a record of £620 billion.

Tom Selby, analyst at AJ Bell, says the spike in cash accounts is understandable in the context of last year’s pandemic, when risk aversion and holding liquid assets would have been a sensible strategy. “Those who held a significant proportion of their ISA in cash might have felt like they had dodged a bullet in March and April last year, when markets tanked as the UK entered its first lockdown,” he says.

But he points out that those holding cash would have missed out the strong bounceback in global shares from the March lows. From trough to peak, the FTSE 100 is up from 5,190 points in March 2020 to 7,129 in May 2021, an increase of 37%. Those putting their Isa allowance into overseas stock markets in the last month of the financial year would have fared even better, with the Dow Jones up 77% from its March nadir. Data from the most recent tax year for 2020/2021, will show whether savers and investors embraced Stocks & Shares Isas as markets recovered.

It will also be interesting to see what happens to this excess cash saved during lockdown, which the Bank of England estimates at around £150 billion, 10% of which consumers are expected to spend.

Inflation and Interest

While cash was the preferred option for 2019/2020, the balance between cash and shares is more even when total figures are taken into account – Cash Isas account for 51% in that year, compared with 49% for Stocks & Shares Isas. Jason Hollands, managing director of Bestinvest, says that for most people Cash Isas are “utterly pointless” because rates on offer are so low and savers can already get tax-free interest by using the Personal Savings Allowance. He also warns that with inflation rearing its head again, the returns on most cash Isas will be negative in real terms. “I urge people to think carefully about the balance they have between shorter term rainy day savings and longer term investments. Cash isn’t king in a world of rising inflation,” he says.

Lifetime Isa (Lisa) accounts more than doubled from the previous tax year to 545,000, from 223,000 in 2018/2019, a boon to the UK Government, which is keen to get more people on to the property ladder and encourage retirement saving habits among the young. Lisas, which came in in the 2017/2018 tax year, regularly feature in our Investor Views column as a way for young people to buy their first property and there’s a full explainer on the terms and conditions in our “What Are Lifetime Isas?” article. AJ Bell’s Selby says the lure of the £1,000 bonus is a big driver in the Lisa’s popularity. Combined with the stamp duty holiday, which was extended in the March 2021 Budget, first-time buyers using their Lisa deposits are having an impact on housing demand and prices, says.

Junior Isas and Cash

Cash remained the preferred option for people saving for their children (and grandchildren), with cash Junior Isas making up 61% of the year’s total. BestInvest’s Hollands says this isn’t just a Covid-19 trend, with the proportion of Cash Isas taken out hovering between 67% and 72% since the Jisa was unveiled nearly 10 years ago. Equities should be the go-to asset class for children, Hollands says.

“In most cases, Junior ISAs are going to be very long-term schemes, which lend themselves to funds investing in stocks and shares, not cash where the real value will just be eroded over time by the corrosive effect of inflation,” he says.

As part of our recent Isa season special report, we wrote a full explainer on how Junior Isas work and the pros and cons of using them to provide for children’s futures.